Regional Trade Policies Impacting Power Equipment Costs

Regional trade policies are driving up power equipment costs and creating supply chain delays. The United States, Europe, and Asia-Pacific are all navigating these challenges differently:

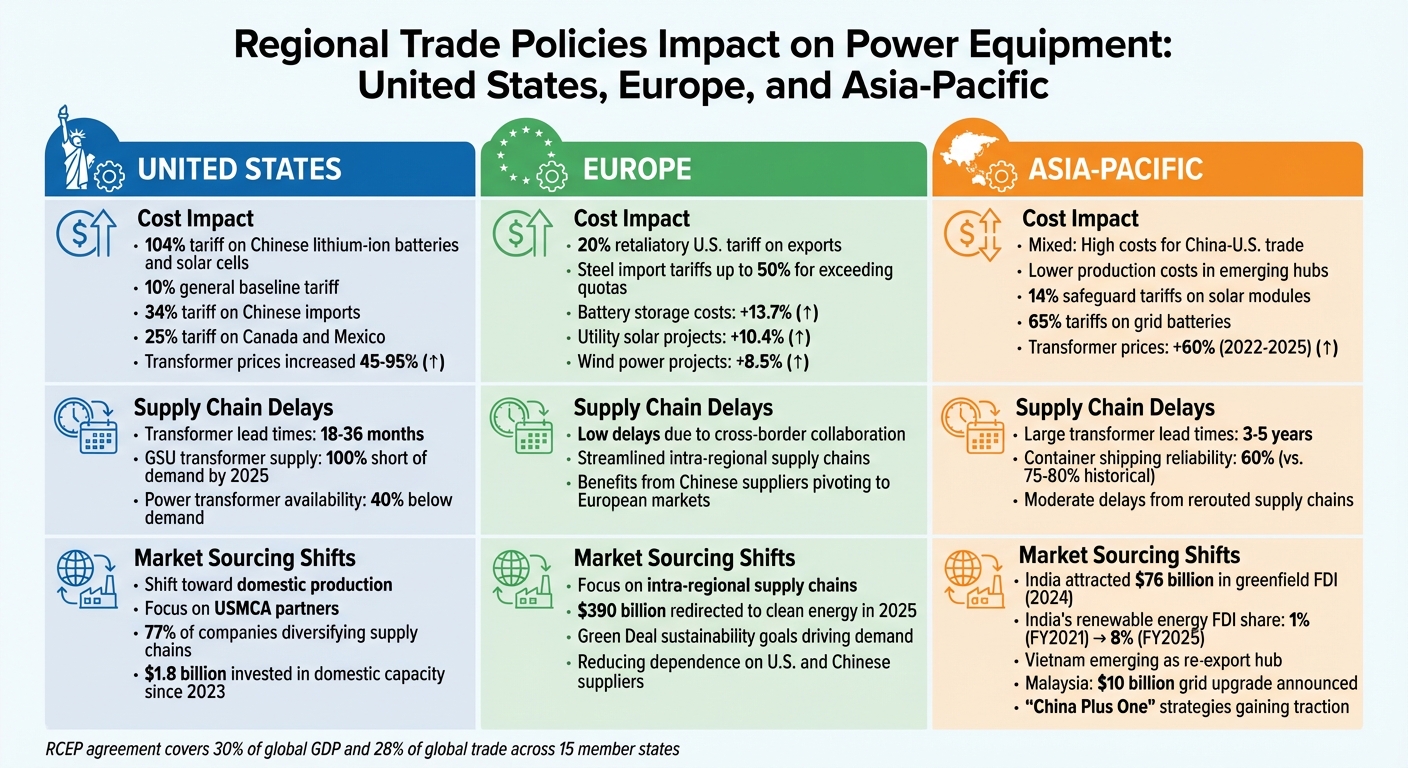

- U.S. tariffs on imports (up to 104%) are raising prices for transformers, cables, and other equipment. Lead times for transformers now stretch up to 36 months.

- Europe faces rising costs due to tariffs on key materials but benefits from streamlined intra-regional supply chains.

- Asia-Pacific sees mixed impacts, with reduced tariffs under agreements like RCEP but persistent shipping delays and reliance on Chinese rare earth metals.

Businesses are responding by shifting sourcing strategies, investing in domestic production, and exploring secondary markets to manage costs and delays. Transformer prices alone have increased by 45–95% since 2020, forcing utilities and contractors to rethink procurement strategies.

For buyers, platforms like Electrical Trader offer access to both new and used equipment, helping to bridge gaps caused by long lead times and rising costs.

Market Day Report: Supreme Court strikes major blow to President Trump's tariff trade strategy

sbb-itb-501186b

1. US Tariffs on Power Equipment

U.S. tariffs on power equipment are part of broader trade policy trends, offering a glimpse into how various markets adapt to similar challenges.

Cost Impact

By March 2025, tariffs on imports from Mexico and Canada hit 25%, while duties on Chinese goods climbed from 10% to 20%, bringing the average tariff on power equipment to 23.5%. These increases target essential materials like grain-oriented electrical steel, aluminum, and electronic regulators, leaving manufacturers with a tough choice: absorb the extra costs or pass them on to consumers.

In April 2025, Stanley Black & Decker responded with a single-digit price hike for its U.S. Tools & Outdoor division. CEO Donald Allan, Jr. also launched a 12–24-month plan to reduce dependence on China, shifting toward North American production, which already accounts for 60% of the company’s U.S. cost of sales. These changes are expected to reduce 2025 earnings per share (EPS) by $0.75. Other manufacturers followed suit, raising prices by 10% to 15.3% to offset the tariff burden.

The ripple effects are being felt across industries. Utilities are warning about higher costs delaying critical projects. Paul Patterson, an equity analyst at Glenrock Associates, cautioned:

"If infrastructure becomes more expensive to build, utilities may face pressure to delay projects".

The National Association of Home Builders predicts that new home prices could rise by over $9,000 due to the cumulative impact of tariffs on construction and electrical materials. These cost increases are also causing significant disruptions in supply chains.

Supply Chain Delays

Lead times for Generation Step-Up (GSU) and power transformers have stretched from months to years. By 2025, GSU transformer supplies are expected to fall nearly 100% short of demand, while power transformer availability lags by 40%. Sub-supplier tariffs are compounding these delays, as manufacturers struggle to find compliant vendors.

Gas turbine prices have soared, more than doubling in recent years, as production struggles to meet the growing demand from AI data centers. In February 2025, FirstEnergy and American Electric Power filed risk disclosures with the SEC, highlighting concerns that tariffs on Canada and Mexico could disrupt supply chains, delay infrastructure repairs, and increase capital costs for fleet modernization.

These challenges are pushing manufacturers to rethink their sourcing strategies to mitigate risks.

Market Sourcing Shifts

Manufacturers are increasingly looking beyond China, turning to USMCA countries and emerging markets like India and Southeast Asia. For example, Polaris announced in May 2025 that it plans to cut sourcing from China by 30% by the end of the year. CEO Michael Speetzen emphasized the company’s focus on boosting USMCA-qualified shipments and managing internal costs rather than resorting to immediate price increases.

Similarly, Hitachi Energy committed $22.5 million to expand dry-type transformer production in southwest Virginia as part of a $250 million global initiative, with 40% of the investment directed at U.S. operations to reduce lead times. Meanwhile, about 30% of CFOs in the construction and utilities sectors are actively working to diversify supply chains to reduce tariff exposure.

These shifts highlight the growing urgency to adapt sourcing strategies in response to rising costs and supply chain uncertainties.

2. Asia-Pacific Trade Dynamics

As U.S. tariffs tighten domestic markets, the Asia-Pacific region is navigating a different landscape. While tariffs in this region are being reduced, other hurdles like extended delivery times and safeguard tariffs present unique challenges. Unlike the U.S., where tariffs directly drive costs up, Asia-Pacific markets are finding a balance between tariff reductions and logistical obstacles.

The Regional Comprehensive Economic Partnership (RCEP) is playing a key role in reshaping trade in power equipment across the region. This agreement spans 15 member states, collectively representing over 30% of global GDP and 28% of global trade. It aims to phase out tariffs on more than 90% of goods over the next 20 years. The biggest winners? Machinery, electrical equipment, and electronic products, which see the steepest tariff cuts, directly influencing the cost of power distribution equipment.

Cost Impact

RCEP’s tariff reductions are expected to significantly boost trade within the region. Intra-regional exports could rise by around $42 billion, with Japan alone projected to see a 5.5% increase in exports - roughly $20 billion compared to 2019 levels. For instance, 87% of Japan's auto parts exports to China will eventually face lower or zero tariffs. But there's a downside for non-members: the United Nations Conference on Trade and Development (UNCTAD) estimates that about $25 billion of the export growth may result from trade being diverted away from countries outside the agreement.

The agreement’s "Rule of Origin" offers flexibility, allowing products to qualify for duty-free treatment if 40% of their components come from any RCEP member. This is a more relaxed requirement compared to the 60% threshold in agreements like the USMCA. Such leniency motivates importers to source components from RCEP countries, including Vietnam, Thailand, and Malaysia. Yet, even with these benefits, global transformer prices have surged by over 60% between 2022 and 2025, driven by commitments to renewable energy projects and supply shortages. Copper alone accounts for 10-20% of production costs.

While tariff reductions offer clear advantages, they are offset by persistent supply chain delays.

Supply Chain Delays

The Asia-Pacific region’s supply chains are grappling with serious bottlenecks. Lead times for large transformers over 500 MVA have stretched to an average of 3 years, with some suppliers quoting up to 5 years. Container shipping reliability also remains a concern, with on-time arrivals hovering just above 60% in late 2025, far below the historical norm of 75-80%. On top of that, Southeast Asia faces steep tariffs on solar power components, including 14% safeguard tariffs on modules and cells, while grid batteries are hit with tariffs of around 65%.

Chris Seiple, Vice Chairman of Energy Transition and Power & Renewables at Wood Mackenzie, highlighted the consequences of these delays:

"The inability to connect load quickly enough is likely to result in greater geographic dispersion of data-centre growth. Indeed, this growth may not materialize – not because it does not exist, but because utilities cannot move quickly enough".

In response, companies are adjusting their sourcing strategies to navigate these challenges.

Market Sourcing Shifts

India is emerging as a key alternative to China for manufacturing investments. In 2024, India attracted $76 billion in greenfield FDI, marking a 13% increase, while China’s FDI saw a second consecutive annual decline, dropping by 29%. India’s share of renewable energy-related FDI grew from 1% in FY2021 to 8% by FY2025. By 2030, annual grid investments in both China and India are expected to exceed $300 billion, with a projected 10-year compound annual growth rate (CAGR) of over 12%.

Vietnam has become a vital re-export hub, assembling Chinese parts for Western markets, while Malaysia has announced a $10 billion grid upgrade focused on semiconductors and national infrastructure. Christina Lee, Head of Asia Content at Macquarie Capital, commented:

"Asia's role as the high-end manufacturer of innovations will continue – and could even step up this year in light of the geopolitical landscape".

This shift reflects the growing adoption of "China Plus One" strategies, where companies diversify manufacturing across Southeast Asia to reduce tariff exposure and supply chain risks. These regional trade policies are directly influencing how power equipment is sourced and priced.

3. European and North American Trade Policies

U.S. trade policies lean heavily on high tariffs to encourage domestic production, while Europe focuses on securing steady supplies amidst global disruptions. These contrasting strategies are reshaping how power equipment is priced and sourced in both regions.

Cost Impact

As of April 2025, the U.S. has enacted a general 10% tariff on most imports, with even steeper rates - 34% for China and 25% for Canada and Mexico. Meanwhile, the EU faces 20% tariffs on key materials like steel, aluminum, and semiconductors, all essential for power distribution equipment.

The impact? Significant cost increases across the board: battery storage costs are up by 13.7%, utility-scale solar by 10.4%, and wind power by 8.5%. Transformer prices are expected to jump another 20% to 30%. For instance, a 50% tariff on copper can add $50,000 to $200,000 to the price of a single large transformer. Some transformer units now cost 150% more than they did in 2020.

"Achieving self-sufficiency in transformer production will take decades and billions in investment".

Benjamin Boucher, Senior Analyst at Wood Mackenzie, highlighted a stark reality: the U.S. manufactures only 20% of the transformers it uses, importing the remaining 80%. "Made in America" policies further complicate matters by preventing utilities from sourcing cheaper equipment from Canada or Mexico when domestic supply struggles to meet demand. Europe, on the other hand, remains highly dependent on imported energy technologies, making it vulnerable to price shocks triggered by U.S. trade actions.

| Equipment/Resource | Impact of U.S. Tariffs on Cost |

|---|---|

| Battery Storage Projects | +13.7% |

| Utility Solar Projects | +10.4% |

| Wind Power Projects | +8.5% |

| Lithium-ion Batteries | +25% (projected) |

| Steel and Aluminum | +$300 per tonne |

These cost increases are compounded by significant delays across supply chains.

Supply Chain Delays

Trade restrictions are causing major bottlenecks. For example, gas turbine prices have more than doubled as production struggles to keep up with data center demand. A critical issue lies in the availability of Grain-Oriented Electrical Steel (GOES), essential for transformer cores. With only one domestic supplier and limited production due to trade restrictions, GOES prices have nearly doubled since 2020, now accounting for 25% to 30% of a transformer's material costs.

Tensions are rising: Canada has threatened to limit energy exports from Ontario to the U.S., while the EU is preparing counter-actions against the 20% U.S. tariffs on essential materials. This back-and-forth of retaliatory tariffs is creating market instability, making long-term planning increasingly difficult.

Market Sourcing Shifts

While Asia-Pacific regions benefit from reduced tariffs that ease logistics, North America faces rising costs tied to protectionist policies. Europe, meanwhile, is investing heavily in public projects. In the U.S., 77% of companies are diversifying their supply chains to mitigate geopolitical risks, with 39% planning to shift import sources. Since 2023, major manufacturers have committed $1.8 billion to expand domestic capacity, though these efforts won't immediately balance the market.

In April 2025, Hitachi Energy announced a $22.5 million investment to produce dry-type transformers in Virginia as part of a $250 million global initiative. GE Vernova is putting $600 million into its factories in Florida and Pennsylvania for high-voltage equipment production. Cleveland-Cliffs Inc. launched a $150 million project in July 2025 to convert a shuttered plant in West Virginia into a transformer manufacturing facility.

"The tariffs could make it more expensive to build here and, in some cases, cheaper for our customers to source from outside of the U.S."

Travis Edmonds, Vice President of Supply Chain at Hitachi Energy, underscored this dilemma.

Europe is taking a different route, redirecting $390 billion in 2025 toward clean energy and defense to reduce dependence on U.S. and Chinese suppliers. While the U.S. leans on tariffs to encourage reshoring, Europe is betting on large-scale public spending to achieve greater independence in clean technology. Some U.S. utilities are even adopting Department of Energy-approved transformer designs that bypass GOES tariffs, though these units are less efficient during peak loads.

Western manufacturers report lead times of 3–4 years for large transformers, while Chinese suppliers can deliver in under a year. For buyers navigating these challenges, platforms like Electrical Trader (https://electricaltrader.com) offer access to both new and used power distribution equipment, helping to fill supply gaps when delays hit traditional sourcing channels.

These developments are setting the stage for continued market adjustments across regions.

Pros and Cons

Regional Trade Policy Impact on Power Equipment: Costs, Delays, and Sourcing Shifts

Trade policies across the U.S., Europe, and Asia-Pacific create unique opportunities and challenges for buyers of power equipment. In the United States, protectionist tariffs are a major factor, with a 104% levy on Chinese lithium-ion batteries and solar cells, along with a 10% general tariff, significantly increasing production costs for items like voltage regulators, UPS systems, and harmonic filters. On top of that, transformer lead times have stretched to 18–36 months, making procurement a long and costly process.

Europe faces its own set of hurdles and benefits. While higher export costs - partly due to a 20% retaliatory U.S. tariff - add financial strain, the region benefits from streamlined supply chains. The steady demand driven by Green Deal sustainability goals helps stabilize local markets. Additionally, as Chinese suppliers pivot toward Europe, lead times are reduced, and availability improves. However, steel import tariffs of up to 50% for exceeding quotas still inflate production costs.

The Asia-Pacific region presents a mixed scenario. China dominates in refining critical materials, processing over 85% of the world's rare earths and 70% of its lithium, which keeps base manufacturing costs low. However, U.S. tariffs have forced Chinese exporters to reroute shipments through countries like Vietnam and Malaysia, while focusing more on European and Southeast Asian markets. Meanwhile, emerging markets such as India and Southeast Asia are gaining traction as cost-effective alternatives. Initiatives like India’s Smart Grid Mission are helping these regions grow, though moderate delays persist as supply chains adjust to these shifts.

Here’s a quick breakdown of the regional trade impacts:

| Region | Cost Impact | Supply Chain Delays | Market Sourcing Shifts |

|---|---|---|---|

| United States | High tariffs (104% on key Chinese components; 10% baseline) | Extended lead times (18–36 months for transformers) | Shift toward domestic production and USMCA partners |

| Europe | Moderate - rising export costs due to a 20% retaliatory tariff | Low delays aided by cross-border collaboration | Focus on intra-regional supply chains to meet Green Deal targets |

| Asia-Pacific | Mixed - high costs for China–U.S. trade versus lower production costs in emerging hubs | Moderate delays from rerouted Chinese supply | India and Southeast Asia emerging as primary global investment hubs |

For U.S. buyers dealing with long lead times and rising prices, platforms like Electrical Trader can help. They provide access to a broad selection of new and used power distribution equipment, offering much-needed flexibility when traditional supply channels are under strain. Ultimately, each region's trade policies bring their own blend of cost pressures and supply chain challenges, making strategic sourcing decisions more important than ever.

Conclusion

Regional trade policies are shaking up power equipment costs and availability, pushing the industry to act quickly. In the U.S., tariffs of 34% on Chinese imports and 25% on goods from Canada and Mexico have caused significant delays in transformer production. Meanwhile, Europe’s 20% tariff on critical inputs has led to efforts to simplify supply chains within the region. Across the Asia-Pacific, countries are exploring alternative trade routes and tapping into emerging hubs like India and Southeast Asia, where manufacturing remains cost-effective.

The cost impact is hard to ignore. Manufacturers are passing these tariff-driven increases directly to buyers, with transformer prices jumping by 45–95%, depending on specifications. Peter Londa, President & CEO of Tantalus, summed it up by saying:

"It is unlikely that transformer manufacturers will absorb the cost of tariffs... manufacturers are likely to offload the increases in costs to buyers"

This situation is forcing utilities and contractors to redirect budgets away from vital maintenance and modernization projects just to secure essential equipment. With costs climbing so steeply, it's clear that supply strategies need an overhaul.

To address these challenges, companies must focus on diversifying suppliers, exploring alternative transformer designs, and using real-time analytics to manage costs. These steps are especially critical given the anticipated shortages - 30% for power transformers and 10% for distribution units. Traditional supply channels alone won't cut it anymore.

Platforms like Electrical Trader have stepped in to connect buyers with both new and reconditioned inventory, helping to bypass long manufacturing delays. Over the past year, prices for used transformers have risen by about 20%, making surplus equipment a valuable option for keeping projects on track. However, as Doug Houseman, Senior Managing Consultant at 1898 & Co., warned:

"There is a limit to used or remanufactured equipment at the very large size, and those supplies are being drawn down by industrial customers, Bitcoin and renewables. We may hit the wall on used equipment in the next two to three years"

High tariffs will likely continue to shape cost and availability concerns across global markets. Success in this landscape depends on proactive planning, broadening sourcing options, and making use of every possible resource - including secondary markets. Adapting to these trade challenges is no longer optional - it’s essential for staying ahead.

FAQs

How can I reduce tariff-driven cost increases when buying transformers and switchgear?

To handle tariff-related cost hikes, it's important to keep up with both current and upcoming tariffs. This knowledge allows you to plan your purchases wisely. Consider diversifying your suppliers to reduce dependency on any single source, stockpiling critical components when possible, and keeping an eye on market trends to place orders at the right time. Tools like Electrical Trader can be useful for finding a range of equipment, which might help you sidestep certain tariff-related expenses. The combination of careful planning and supplier diversification can go a long way in lessening the financial strain caused by tariffs.

What should I do if transformer lead times are 18–36 months (or longer) for my project?

To tackle transformer lead times stretching from 18 to 36 months - or even longer - it’s crucial to plan proactively. Place orders well in advance and adjust both your project timelines and budgets accordingly. You might also want to explore alternative suppliers or sourcing from different regions, and even look into reshoring or local manufacturing as potential solutions. Staying updated on market trends and supply chain shifts can help you adapt more effectively. These strategies can reduce delays and keep your project moving forward.

When does buying used or reconditioned equipment make sense, and what are the risks?

Buying used or refurbished power equipment can be a smart choice when you're trying to save money, especially for projects with tight budgets. It’s a practical move as long as the equipment has been properly maintained, thoroughly tested, and inspected for reliability.

That said, there are some risks involved. Used equipment might show signs of wear, raise safety concerns, or lack modern features. To minimize these risks, check maintenance records, perform detailed inspections, and buy only from trusted sellers. This way, you can ensure both safety and good value.