Power Equipment Supply Chains: Regional Challenges

The global supply chain for power equipment is under pressure due to rising demand for renewable energy, aging infrastructure, and geopolitical tensions. Key issues include:

- Soaring Costs: Transformer prices have increased 4–6 times since 2022.

- Long Lead Times: Delivery delays for large transformers now stretch up to 210 weeks (nearly 4 years).

- Material Shortages: Limited availability of grain-oriented electrical steel (GOES), copper, and other key inputs.

- Regional Disparities: North America faces transformer shortages, Europe struggles with raw material access, and Asia-Pacific deals with production bottlenecks and tariffs.

Efforts like domestic manufacturing investments and digital procurement platforms are helping to ease these challenges, but systemic bottlenecks remain. Addressing these issues is critical to meeting growing energy demands and decarbonization goals.

North America: Transformer Shortages and Extended Lead Times

Demand Pressures from Aging Infrastructure and Data Centers

The U.S. power grid is grappling with a surge in demand driven by multiple factors. First, a staggering 55% of the 60–80 million transformers in use are over 33 years old, surpassing their intended lifespans. Second, the push for decarbonization and the widespread adoption of electric vehicles and heat pumps are introducing significant new loads to the system. Third, the rapid expansion of AI data centers and cryptocurrency mining has created an extraordinary need for three-phase, dry-type transformers.

Richard Voorberg, President of Siemens Energy North America, highlighted the unprecedented nature of this shift:

"I've been in this industry for 32 years... I've never seen something like this that is going up at such a rate that looks sustainable as well"

. Between 2019 and 2025, the demand for generation step-up (GSU) transformers skyrocketed by 274%, while substation power transformer demand increased by 116% during the same period. Looking further ahead, capacity requirements for distribution transformers could rise by as much as 260% by 2050 compared to 2021 levels.

This surge in demand has created significant challenges for manufacturers, leading to widespread delays.

Lead Time Delays and Manufacturing Constraints

The sharp increase in demand has exposed critical bottlenecks in transformer production, resulting in significant delivery delays. Average lead times now range from 128 to 143 weeks, with some large power transformers taking as long as 210 weeks - nearly four years - to deliver, a stark contrast to the pre-pandemic norm of 30–60 weeks.

A major contributing factor is the limited availability of key materials. The U.S. has just one domestic supplier of Grain-Oriented Electrical Steel (GOES) - Cleveland-Cliffs - leading to material shortages. Since the pandemic, GOES prices have doubled, and copper costs have surged more than 40%. The manufacturing process itself is labor-intensive, requiring skilled workers who are increasingly hard to find. Adding to the delays, transporting large power transformers - each weighing 100 to 400 tons - requires specialized super-heavy-load railcars. With only about 10 such railcars available nationwide, transportation alone can add months to delivery timelines.

Manufacturers are attempting to address these challenges with significant investments. In September 2025, Hitachi Energy committed over $1 billion to U.S. manufacturing, including $457 million for a new large power transformer facility in South Boston, Virginia, and $106 million for component production in Alamo, Tennessee. Similarly, Siemens Energy announced a $150 million expansion of its Charlotte, North Carolina facility in February 2024, aiming to produce 57 large power transformers annually by the end of 2026. In November 2025, Hyosung HICO pledged $157 million to expand its Memphis, Tennessee plant.

However, these efforts may not be enough to resolve the deeper supply chain issues. Morgan Bazilian, Professor of Public Policy at the Colorado School of Mines, explained the ongoing challenges:

"Until the underlying supply-chain choke points - steel, copper, insulation materials and heavy transport - expand meaningfully, utilities are managing reliability not through construction, but through choreography"

. The stakes are high, with roughly 25% of global renewable projects facing delays due to transformer shortages, underscoring the immense pressure on North America's supply chain.

Europe: Raw Material Shortages and Sustainability Regulations

Impact of Raw Material Shortages on Equipment Production

While North America grapples with transformer delays, Europe faces its own unique supply chain challenges. One of the biggest hurdles? Access to raw materials. For the European Union, having a steady supply of critical raw materials is essential to meet its energy and digital goals. To tackle this, the EU is conducting a comprehensive analysis of its supply chain - from raw materials all the way to finished products - to identify and address potential bottlenecks.

A foresight study is helping map out material demand risks through 2050. This forward-looking approach aims to uncover vulnerabilities that could disrupt equipment production in the long run. As highlighted by the Publications Office of the EU:

"This study contributes scientific evidence to underpin the Critical Raw Materials Act... to identify bottlenecks and to pinpoint the segments of supply chains which need strengthening and how"

.

Sustainability Mandates and Supply Chain Impacts

On top of material shortages, Europe's sustainability regulations are adding another layer of complexity to its supply chain. A major shift is underway as grid operators push for net-zero plans, including the elimination of SF6 (sulfur hexafluoride) - a potent greenhouse gas commonly used in electrical switchgear. This change is forcing manufacturers to rethink how they design and produce equipment.

Logistics are another sticking point. Nearly 40% of Europe’s distribution grids are over 40 years old, and electricity consumption is expected to jump by about 60% by 2030. This aging infrastructure, combined with rising demand, means a massive influx of replacement components is urgently needed. According to the European Commission’s December 2025 European Grids Package, upgrading Europe’s electricity grids will require an estimated €584 billion in investments by 2030. To get ahead of potential disruptions, the EU has started making early investments to expand grids and secure equipment before demand peaks.

Asia-Pacific: Production Capacity Bottlenecks and Trade Barriers

Shipping Delays and Production Hesitations

The Asia-Pacific region, long recognized as a manufacturing hub for power equipment, is grappling with significant production and trade challenges. While historically dominant in this sector, the region is now facing severe production capacity constraints. For example, about 80% of the large transformers used in the U.S. have traditionally been sourced from countries such as China and Thailand. However, the surge in global demand - driven by the expansion of AI data centers, industrial electrification, and renewable energy projects - has created a pronounced supply-demand imbalance.

One major roadblock is the limited availability of critical raw materials. Grain-oriented electrical steel (GOES) and copper, essential for manufacturing transformer cores and wiring, are in short supply. Adding to the strain, manufacturers are hesitant to make substantial investments due to uncertainty surrounding tariffs, which could significantly impact their global competitiveness. Cecilio Velasco, Managing Director at KKR, highlighted this issue:

"Some transmission manufacturers 'remain cautious on investment commitments,' partly due to the uncertainty over tariffs that can have a significant impact on the global competitiveness of their products".

Transportation challenges further compound the issue. Moving large power transformers, which can weigh between 100 and 400 tons, requires specialized heavy-load railcars, leading to extended delivery times. Consequently, lead times for large power transformers in the Asia-Pacific region have stretched to as much as 210 weeks - nearly four years - by 2024. Hitachi Energy’s order book reflects similar delays, with medium-sized units taking up to 130 weeks and the largest utility substation units facing backlogs of nearly four years. These logistical and production challenges are further exacerbated by shifting international trade policies.

U.S. Tariffs and Rising Import Costs

On top of production hurdles, the Asia-Pacific region is now contending with escalating trade restrictions that are adding strain to already stressed supply chains. U.S. tariffs on transformers and related components from key suppliers like China and South Korea are driving up procurement costs and reshaping trade dynamics. The average tariff on utility-scale equipment has climbed to 23.5%, fueled by new duties on copper and imports from various regions. As a result, copper wiring prices have risen by 18% since January 2025, and electrical panels now cost 22% more due to the combined impact of steel and copper tariffs.

The ripple effects are substantial. A reported 82% of supply chain leaders have been impacted by these new tariffs, with 38% planning to scale back their operations in China. This has led to a shift in trade priorities, with countries like Taiwan and Indonesia emerging as alternative suppliers. Some manufacturers, however, are taking a different route altogether. In November 2025, South Korean power equipment giant Hyosung HICO announced a $157 million investment to expand its transformer plant in Memphis, Tennessee. This move reflects a broader trend of Asia-Pacific firms establishing manufacturing operations in the U.S. to sidestep tariffs and meet the skyrocketing demand for generation step-up transformers, which has surged by 274% since 2019.

David Long, CEO of the National Electrical Contractors Association (NECA), underscored the challenges posed by these trade policies:

"The electrical construction industry may face considerable risks due to these tariffs. Employers and industry stakeholders should adopt a proactive approach to mitigate risks associated with these trade policies".

Solutions to Overcome Regional Supply Chain Challenges

Diversified Sourcing and Online Marketplaces

With delays stretching timelines and costs climbing, the industry is shifting toward a mix of digital tools and local manufacturing to tackle supply chain hurdles. The old model of depending on a small group of Tier 1 suppliers is proving unsustainable, especially when 98% of executives cite operational issues as significant disruptors to supply chains. Multi-year backlogs for items like transformers and breakers mean utilities and contractors need quick alternatives to avoid derailing their projects.

Online marketplaces such as Electrical Trader are stepping in to fill this gap by offering access to the secondary market. This includes used, refurbished, and surplus equipment - an increasingly vital resource. While waiting years for new orders isn't an option, these platforms often provide surplus inventory that's ready to go. For electrical contractors working under tight deadlines, finding a refurbished transformer or breaker through a digital marketplace can be the difference between staying on track and facing costly delays. Plus, this approach gives existing assets a second life, sidestepping the lengthy waits tied to new manufacturing.

Another advantage of digital procurement platforms is improved visibility across the supply chain. Only 13% of electric power executives report having insight beyond Tier 2 suppliers, but centralized marketplaces make it easier to search for equipment across regions. Whether you're looking for a pad-mount transformer, medium-voltage switchgear, or specialized breakers, platforms like Electrical Trader bring together options from various sellers into one easy-to-navigate interface. This streamlines procurement and broadens sourcing options, providing flexibility and efficiency. These digital solutions also complement investments in local production, creating a well-rounded approach to securing supply chains.

Localized Manufacturing and Early Procurement

In addition to digital sourcing, boosting domestic manufacturing is a long-term strategy to ease supply chain bottlenecks. Companies like Hitachi Energy and Schneider Electric are making major investments to expand U.S. production. Hitachi Energy has committed $1.5 billion globally, with $500 million earmarked for North America, while Schneider Electric is investing $700 million across Tennessee, Missouri, and Ohio. In April 2025, MGM and VanTran Transformers launched a 30,000-square-foot facility in Waco, Texas, adding $1 billion in annual transformer production capacity.

These domestic manufacturing efforts not only reduce the impact of tariffs but also cut down on transportation challenges. Still, even with increased production capacity, early procurement remains critical. Utilities are now reserving manufacturing slots three to six years in advance to ensure they can meet future demand.

sbb-itb-501186b

Lots More on America's Electrical Components Crisis | Odd Lots

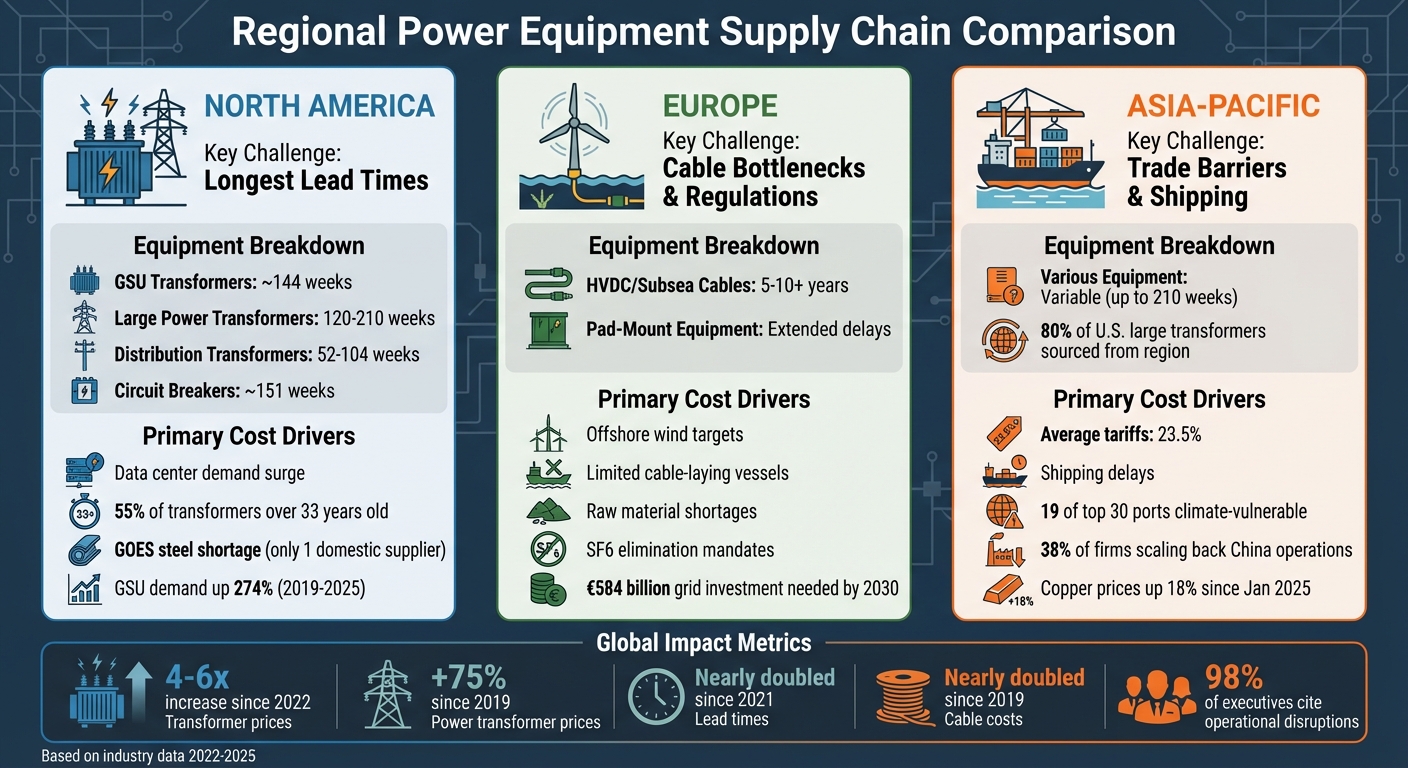

Regional Lead Times and Cost Drivers Comparison

Power Equipment Lead Times and Cost Drivers by Region

Expanding on earlier discussions about supply chain disruptions, this section dives into how lead times and cost drivers vary across major markets. Understanding these differences is crucial for contractors and utilities aiming to fine-tune their procurement strategies. North America faces the longest lead times, with Generator Step-Up (GSU) transformers taking up to 144 weeks - nearly three years from order to delivery. Large power transformers have lead times ranging from 120 to 210 weeks, while high-voltage circuit breakers average around 151 weeks. Even distribution transformers, which used to take only 23 weeks, now require 1 to 2 years for delivery. These delays stem from aging infrastructure and material shortages, creating significant challenges for the region.

In Europe, specialized cables for offshore wind projects are the biggest bottleneck. High-voltage direct-current (HVDC) and subsea cables often take more than 5 years to procure, with some orders stretching beyond 10 years. Pad-mount equipment also faces delays due to raw material shortages and strict sustainability regulations. Globally, lead times for critical grid components like transformers and cables have nearly doubled since 2021, while the cost of cables has almost doubled since 2019.

While Asia-Pacific remains a manufacturing powerhouse, shipping delays, trade restrictions, and U.S. component shortages are forcing companies to seek quicker alternatives from overseas suppliers. The region’s ports face significant climate-related risks - 19 of the world’s top 30 ports are highly vulnerable to extreme weather, most of which are located in Asia-Pacific. Additionally, rising tariffs are prompting a shift in procurement to lower-tariff regions such as Taiwan and Indonesia.

Lead Time and Cost Comparison Table

Here’s a snapshot of how lead times and cost drivers differ across regions:

| Region | Equipment Type | Lead Time | Primary Cost Drivers |

|---|---|---|---|

| North America | GSU Transformers | ~144 weeks | Data center demand, aging infrastructure, GOES steel shortage |

| North America | Large Power Transformers | 120–210 weeks | Manufacturing constraints, component shortages |

| North America | Distribution Transformers | 52–104 weeks | Aging infrastructure, residential growth |

| North America | Circuit Breakers | ~151 weeks | Fault protection needs, production bottlenecks |

| Europe/Global | HVDC/Subsea Cables | 5–10+ years | Offshore wind targets, limited cable-laying vessels |

| Europe | Pad-Mount Equipment | Extended | Raw material shortages, sustainability mandates |

| Asia-Pacific | Various Equipment | Variable | Shipping delays, tariffs (avg. 23.5%), trade barriers |

Transformer prices have skyrocketed, increasing 4 to 6 times compared to pre-2022 levels. Globally, power transformer prices have jumped 75% since 2019. Meanwhile, tariffs have driven up costs for battery storage projects by 13.7%, utility solar by 10.4%, and wind energy by 8.5%. Gas turbine prices have doubled as manufacturers struggle to meet the 24/7 electricity demands of data centers. These challenges are pushing buyers to explore alternative sourcing strategies to manage delays and rising costs effectively.

Conclusion

Power equipment supply chains are grappling with regional challenges that demand strategic shifts. Transformer prices, for instance, have skyrocketed to four to six times their pre-2022 levels. Surveys reveal a growing focus on operational adjustments and strategic planning, emphasizing that reactive procurement is no longer enough to navigate these pressures.

To tackle these hurdles, businesses are turning to forward-thinking approaches and smarter risk management. A survey indicates that 39% of companies are adopting dual sourcing strategies, while 45% are increasing inventory levels to buffer against disruptions. As Oliver Wyman aptly states:

"Embedding these practices [visibility and risk diversification] is no longer optional, but critical for maintaining business continuity and public trust".

Digital platforms like Electrical Trader have emerged as vital tools in this landscape. By broadening vendor pools and reducing lead times from years to weeks, these platforms help alleviate supply chain bottlenecks. This shift toward digital solutions aligns with the broader trend of localizing and diversifying sourcing strategies.

As highlighted in our regional analysis, adapting to specific local challenges is key to staying competitive. With major supply chain adjustments anticipated over the next three years, strategies like nearshoring, improved supplier visibility, and sourcing diversification are proving indispensable. These proactive measures remain the most reliable ways to manage costs and maintain steady lead times.

FAQs

How do digital procurement platforms address challenges in the power equipment supply chain?

Digital procurement platforms are transforming how supply chain challenges are managed in the power equipment sector. By streamlining and accelerating the sourcing process for essential components, these platforms make it easier to access items like transformers, circuit breakers, and other power distribution equipment. This efficiency helps minimize delays caused by manufacturing slowdowns, shipping issues, or surges in demand for specialized products.

With features like real-time inventory updates and data-driven insights into pricing and availability, these platforms bring much-needed transparency to the procurement process. Businesses can make smarter purchasing decisions, better manage costs, and focus on acquiring critical equipment when it's most needed. Beyond that, these tools also contribute to strengthening domestic manufacturing efforts and reducing dependence on international supply chains, bolstering the resilience of the industry as a whole.

What causes long lead times for power transformers?

The long wait times for power transformers stem from a mix of challenges. One major factor is the limited manufacturing capacity within the U.S., which forces a heavier reliance on overseas suppliers. This reliance becomes problematic when global supply chains encounter disruptions, leading to significant delays.

On top of that, shortages of essential materials such as grain-oriented electrical steel - a key component in transformer production - have added pressure. Rising demand fueled by grid expansion and modernization projects only exacerbates the situation. To make matters worse, the aftershocks of pandemic-related disruptions are still rippling through supply chains, creating bottlenecks that continue to slow down production.

What challenges are regional differences creating for the global power equipment supply chain?

Regional differences are posing serious hurdles for the global power equipment supply chain. In the United States, one of the main concerns is aging infrastructure - more than 70% of transmission and power transformers are over 25 years old. This outdated equipment has fueled a growing need for greater transmission capacity, which is expected to triple by 2050. Adding to the complexity, the heavy reliance on foreign suppliers leaves the supply chain exposed to risks like international conflicts, tariffs, and global shortages. These factors can cause shipment delays and drive up costs for critical components such as transformers.

To tackle these issues, there’s a push to strengthen domestic manufacturing. Investments in new production facilities and the use of government programs, such as the Defense Production Act, are part of these efforts. Still, challenges persist, as differences in infrastructure conditions, economic capabilities, and geopolitical stability vary widely across regions. To build a more reliable and efficient global power distribution network, strategies like diversifying suppliers and adopting localized solutions are becoming increasingly necessary.