Hydrogen Power Investments: Risks and Rewards

Hydrogen power is gaining traction as a critical energy solution for industries that can't rely on batteries, like steel production, heavy-duty trucking, and aviation. By 2050, hydrogen could meet up to 18% of global energy needs. However, investing in hydrogen comes with challenges like high upfront costs, fluctuating prices, and regulatory uncertainty. Here's what you need to know:

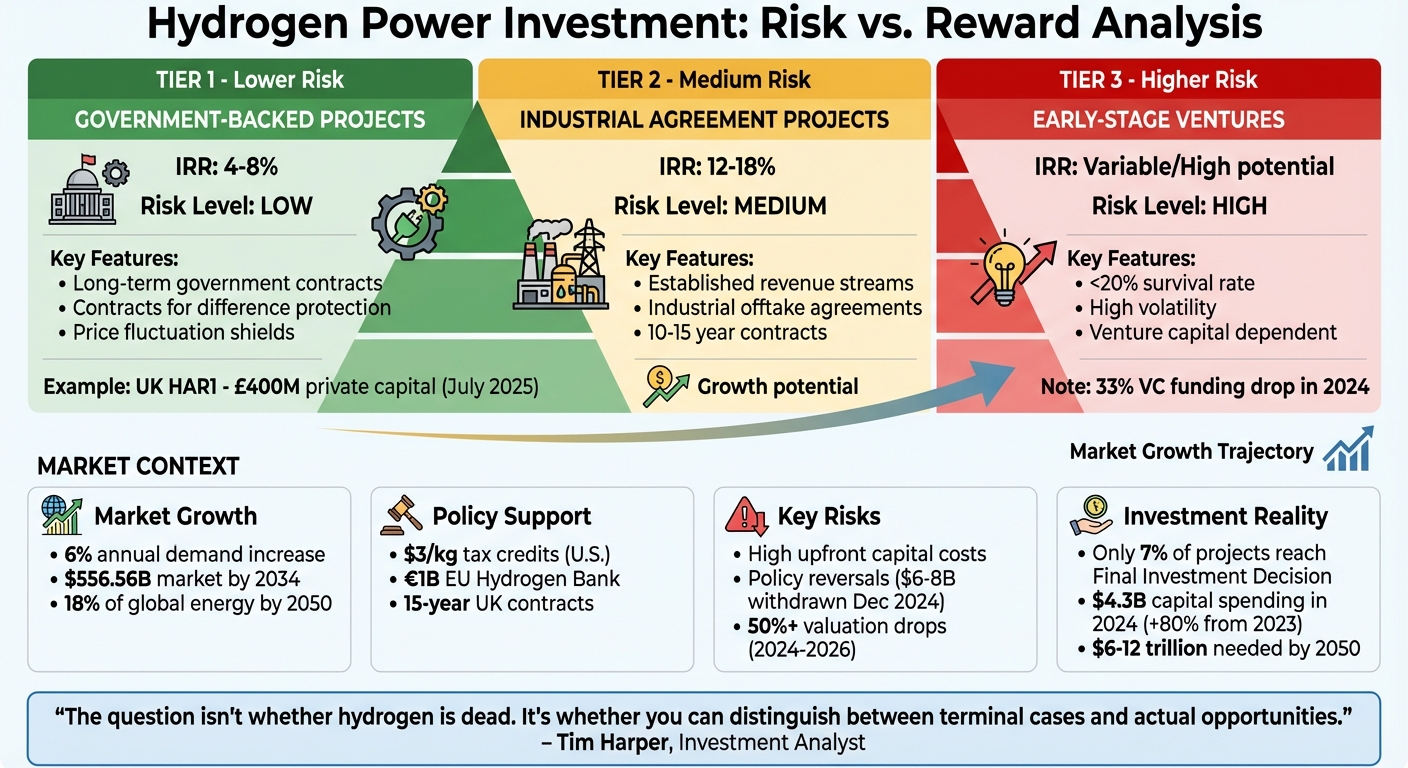

- Global hydrogen market: Expected to grow from $262.13 billion in 2024 to $556.56 billion by 2034.

- Government incentives: The U.S. offers up to $3/kg in tax credits, while Europe is funding hydrogen projects through subsidies and auctions.

- Risks: High capital costs, policy changes, and market volatility have led to bankruptcies and valuation drops in recent years.

- Rewards: Projects backed by long-term contracts offer lower risks and stable returns, while advancing technology is reducing production costs.

Hydrogen power presents opportunities but requires careful planning. Focus on financially stable projects, diversify across the hydrogen value chain, and monitor industry developments to navigate this complex market effectively.

Benefits of Investing in Hydrogen Power

Rising Demand for Hydrogen Across Industries

Hydrogen is becoming a go-to solution for industries that lack viable alternatives to reduce emissions. In the U.S. alone, oil refining and chemical production rely on around 10 million metric tons of fossil-based hydrogen annually. Transitioning to clean hydrogen presents a clear opportunity for growth in these sectors. Meanwhile, the transportation sector - responsible for about 25% of energy-related CO₂ emissions - is increasingly adopting hydrogen for applications like heavy-duty trucking, maritime shipping, and aviation, where battery-electric options fall short in range and power.

The steel industry is also making a significant shift by replacing carbon-heavy coking coal with 100% hydrogen-based Direct Reduced Iron (DRI) production. On a broader scale, over 130 governments and a third of Fortune 2000 companies have pledged net-zero commitments, further fueling a demand for ready-to-deploy decarbonization solutions. By 2030, the U.S. is expected to reach an operational clean hydrogen production capacity of 7–9 million metric tons annually.

This growing demand is bolstered by strong government support and financial incentives.

Government Incentives and Tax Credits

The U.S. government is offering significant financial backing to the clean hydrogen sector. Section 45V provides up to $3.00 per kilogram of clean hydrogen over a 10-year period, making green hydrogen projects more economically viable. This tiered credit system rewards production methods with lower lifecycle greenhouse gas emissions. Thanks to this incentive, the cost of green hydrogen could drop from $5.00–$7.00 per kilogram to as low as $0.50–$2.00 per kilogram.

Some major projects are already taking advantage of these credits. Constellation Energy plans to restart operations at Three Mile Island Unit 1 by 2028, qualifying for the highest credit tier. Similarly, Michigan’s Palisades nuclear power plant is set to resume operations by late 2025, creating another pathway for subsidized hydrogen production.

Technology Improvements Reducing Costs

Advances in technology are making green hydrogen production more affordable. Between 2020 and 2026, production costs dropped by about 45%, largely due to improvements in electrolyzer efficiency and scaling. For example, Solid Oxide Electrolyzer Cells (SOECs) now produce 20–25% more hydrogen per megawatt compared to traditional systems, using roughly 37.5 kWh per kilogram of hydrogen instead of the usual 52–54 kWh.

Innovations from companies like Bloom Energy and Honeywell highlight this progress. Bloom Energy’s 4-MW SOEC installation at NASA’s Ames facility and Honeywell’s catalyst-coated membranes, which increase hydrogen output by 55% while lowering PEM stack costs by 35%, showcase the rapid advancements. By early 2026, global electrolyzer manufacturing capacity had reached 61 GW, and every 5 kWh reduction in electricity use per kilogram of hydrogen lowers production costs by $0.20–$0.30 per kilogram. These technological strides make hydrogen an increasingly attractive investment option.

sbb-itb-501186b

Main Risks of Hydrogen Power Investments

Large Upfront Capital Costs

Investing in hydrogen projects demands a hefty initial financial commitment. By 2025, electrolysis-based projects were projected to consume 80% of the capital spending in the sector while delivering just 56% of the production output - highlighting a clear imbalance between investment and returns. In 2024 alone, spending on low-emissions hydrogen projects surged to $4.3 billion, marking an 80% jump from 2023.

Infrastructure challenges, such as delays in grid interconnection and the absence of dedicated pipelines, further drive up costs. Companies like Plug Power exemplify these struggles, with their deficits surpassing $8 billion by 2025. To manage cash flow issues, many firms have turned to issuing more shares or implementing reverse stock splits. For example, FuelCell Energy executed a 1-for-30 reverse split in November 2024 to maintain its stock exchange listing. These financial strains are compounded by unpredictable regulatory landscapes.

Changing Regulations and Policy Delays

Shifting policies can derail hydrogen projects almost overnight. A stark example occurred in December 2024, when the U.S. federal government withdrew $6 billion to $8 billion in hydrogen tax credits via executive order. This abrupt decision led to the immediate cancellation of major projects, including BP's 500MW HyGreen Teesside facility. In total, this policy change contributed to $22 billion worth of canceled or scaled-back clean energy initiatives in 2025.

Adding to the challenges, stringent rules around additionality, hourly matching, and deliverability have significantly increased costs and operational hurdles. As a result, only 7% of the $570 billion in announced hydrogen investments through 2030 have reached the Final Investment Decision stage. Europe has seen its own setbacks, with 33 hydrogen projects representing 3.6 GW of capacity either canceled or paused in 2024 due to regulatory and market uncertainties.

"None of our prospective customers will take an investment decision - even on large-scale development costs - without that level of clarity."

– Tim Calver, Vice President of Commercial, ITM Power

This lack of regulatory stability continues to undermine investor confidence and market growth.

Price Fluctuations and Cash Flow Issues

The unpredictable nature of hydrogen pricing creates revenue instability. Currently, green hydrogen costs between $3 and $6 per kilogram, while conventional grey hydrogen is far cheaper, ranging from $1.50 to $2.50 per kilogram. For green hydrogen to compete effectively, production costs need to drop to between $2.50 and $4.00 per kilogram by 2030.

Market volatility has also taken a toll. Between 2024 and 2026, valuation compressions highlighted the sector's financial fragility. For instance, the HydrogenOne Capital Growth (HGEN) fund saw a staggering 54.1% drop in portfolio value over just four months in 2025. This uncertainty has led investors to demand higher risk premiums, with discount rates soaring from 12.2% to 22.9% in early 2025. Reflecting this skepticism, venture capital funding for hydrogen projects fell by 33% in 2024.

"The market for hydrogen-related technology has weakened significantly over recent months and the lack of funding available to our portfolio companies has clearly demonstrated this."

– HydrogenOne Capital Growth Half-Year Report

The financial struggles of industry players further highlight these risks. In March 2025, Danish electrolyzer manufacturer Green Hydrogen Systems filed for bankruptcy after failing to secure additional funding. Despite raising over $100 million in venture capital, its technology was sold to thyssenkrupp Nucera for just €10–15 million. Similarly, German developer HH2E entered self-administration in November 2024 when its majority shareholder, Foresight Group, declined further investment, leading HGEN to write off its £11 million stake entirely.

Green Hydrogen - Should You Invest Now or Wait?

Comparing Risks and Rewards

Hydrogen Power Investment Risk-Reward Analysis by Project Tier

Hydrogen investments offer a mix of opportunities and challenges, which can be grouped into three distinct tiers. These tiers provide a clearer picture of where potential value aligns with inherent risks.

Tier 1 projects are backed by long-term government contracts, offering lower-risk investments with returns of 4–8% IRR. A notable example is the UK Hydrogen Allocation Round (HAR1), which, in July 2025, attracted $400 million in private capital through contracts for difference that shield producers from price fluctuations. Tier 2 projects, supported by established revenue streams and industrial agreements, target higher returns of 12–18% IRR. Meanwhile, Tier 3 ventures are early-stage and carry the highest risk, with less than a 20% survival rate.

Despite short-term volatility, the long-term potential is striking. Hydrogen demand is expected to grow 6% annually, surpassing 150 million tons by 2030. By 2034, the global hydrogen market could reach $556.56 billion. Looking further ahead, hydrogen could meet 18% of global energy demand by 2050 - an eightfold increase from current levels. Industries like steelmaking, shipping, and aviation, which are harder to decarbonize, stand to benefit significantly as global net-zero goals drive adoption.

However, the financial landscape is not without peril. From late 2024 to early 2026, the hydrogen sector faced a "sector clear out", with valuations plummeting by over 50%. During the same period, venture capital funding dropped by 33%, as investors shifted focus from large-scale funding rounds to survival-stage financing.

"The question isn't whether hydrogen is dead. It's whether you can distinguish between terminal cases and actual opportunities." – Tim Harper, Investment Analyst

This tiered framework helps investors weigh the promise of hydrogen’s growth against the challenges of market volatility. Understanding these distinctions is key to making informed investment decisions.

Risk vs. Reward Comparison Table

| Factor | Potential Rewards | Potential Risks |

|---|---|---|

| Market Growth | 6% annual demand increase; $556.56 billion market by 2034; 18% of global energy by 2050 | Competition from battery technology; adoption uncertainty; high infrastructure costs |

| Policy/Incentives | $3/kg tax credits (U.S. IRA); €1 billion EU Hydrogen Bank; 15-year contracts for difference (UK HAR) | Sudden policy reversals; strict subsidy requirements; regulatory uncertainty |

| Operational | Decarbonization of steel, shipping, aviation; cost reduction target to $1/kg by 2030 (U.S. Hydrogen Shot) | High upfront capital costs; grid connection delays up to 10 years; safety concerns |

| Financial | 12–18% IRR for growth-stage projects with offtake agreements; Air Liquide projects hydrogen revenue growth from €2 billion to €6 billion by 2035 | High cash burn and frequent dilution |

As of May 2024, only 7% of announced electrolytic capacity had reached the Final Investment Decision stage globally, highlighting the significant hurdles that projects face in moving from concept to execution.

How to Invest in Hydrogen Power

These strategies aim to address the steep initial costs and regulatory challenges in hydrogen power, helping investors find a balance between risk and potential rewards.

Focus on Financially Sound Projects

Start by evaluating a project’s financial health. A key metric is the cash burn rate - calculated as operating cash flow minus investing cash flow. Divide total cash reserves by the quarterly burn rate; if the result is less than 18 months, the company might need emergency capital raises, which could dilute shareholder value.

The strength of a company’s order book can reveal its market traction. Firm orders, backed by customer deposits, are far more reliable than non-binding agreements like memorandums of understanding. Look for projects with long-term offtake agreements - typically 10 years or more at fixed prices. These contracts protect producers from market fluctuations and make projects more appealing to investors. For example, the UK's Hydrogen Allocation Round 1 (HAR1) in July 2025 unlocked £400 million in private investments for 10 projects by offering 15-year government-backed revenue guarantees.

Another key factor is intellectual property. Companies with strong patent portfolios in essential technologies - like membrane electrode assemblies (MEAs) or advanced materials - are better positioned to succeed in the long run. Additionally, manufacturing scalability is crucial. Firms moving toward "giga-factory" scale production can meet growing demand and reduce costs.

Once you’ve identified financially strong projects, diversify your investments to reduce risks across the hydrogen ecosystem.

Spread Investments Across Different Applications

Diversification is essential to manage risk effectively. The hydrogen value chain includes three main areas:

- Production (e.g., electrolyzers)

- Infrastructure (e.g., storage, pipelines, refueling stations)

- End-Use Technology (e.g., fuel cells for transportation or industrial power).

By spreading investments across these segments, you can protect against risks tied to specific technologies or regulatory changes.

Geographic diversification is another smart strategy. North America benefits from strong policy backing under the Inflation Reduction Act, Europe has well-established frameworks like the Green Deal, and the Asia-Pacific region - led by China, which accounts for 61% of global hydrogen manufacturing capacity - offers rapid market growth. Additionally, targeting sectors like heavy-duty shipping, steel production, and chemical refining can help secure steady demand.

Monitor Industry Developments

Staying informed gives you an edge. Keep an eye on how technologies progress from pilot stages to full-scale industrial deployment. Tools like Technology Readiness Levels (TRL) can help you track innovations such as microwave plasma pyrolysis and salt cavern storage.

Capital spending on low-emissions hydrogen projects surged to $4.3 billion in 2024, up 80% from 2023, and is expected to reach nearly $8 billion in 2025. Electrolysis accounts for 80% of this investment. Focus on projects that have achieved Final Investment Decision (FID) status, as these have secured engineering, financing, and offtake agreements. By May 2024, global operational green hydrogen capacity reached 1.4GW, with another 20GW at the FID stage.

Government funding rounds, like the UK Hydrogen Allocation Rounds and EU Hydrogen Bank auctions, are also crucial indicators of strong policy support. Additionally, track advancements in electrolyzer technology - costs dropped from $1,200/kW in 2015 to $400–$600/kW in 2024, with a target of less than $200/kW by 2030. These reductions are vital for achieving competitive production costs of $2.50–$4.00/kg compared to conventional fuels.

Lastly, keep an eye on Nationally Determined Contribution (NDC) reviews scheduled for 2025–2027. These reviews often push governments to channel funds into infrastructure projects that are ready to go, helping meet climate goals.

Conclusion

The future of hydrogen power investments hinges on careful planning and well-informed choices. After a period of inflated expectations, the market faced reality between late 2024 and early 2026. This phase brought significant challenges, including bankruptcies like Green Hydrogen Systems and HH2E, as well as notable declines in portfolio values across the sector.

Despite these setbacks, the core market indicators remain promising. In 2024, capital spending on low-emissions hydrogen projects soared to $4.3 billion - an 80% increase from 2023 - and is expected to climb to nearly $8 billion in 2025. Looking further ahead, integrating hydrogen into the global energy system from 2025 to 2050 is expected to require investments ranging from $6 trillion to $12 trillion.

For investors, the most effective approach involves targeting financially stable, government-supported projects with long-term revenue contracts spanning 10–15 years. Diversifying investments across hydrogen production, infrastructure, and end-use applications - particularly in sectors like steel, maritime shipping, and aviation - can also maximize opportunities. These industries are among the most challenging to electrify, making hydrogen a cost-efficient decarbonization solution. Additionally, geographic diversification could lower costs by as much as 21%.

Staying vigilant is key to navigating this evolving sector. Investors should keep a close eye on cash burn rates, track projects that have reached Final Investment Decision status, and remain updated on policy changes, including Nationally Determined Contributions (NDC) reviews and government funding allocations. With hydrogen projected to meet 10% to 18% of global energy demand by 2050, disciplined and patient investors stand to benefit significantly from this transformative energy source.

FAQs

What’s the safest way to invest in hydrogen without betting on a single startup?

Investing in hydrogen ETFs is one of the safest ways to tap into the hydrogen sector. These funds offer a diversified portfolio, reducing the risks associated with putting all your money into a single company. By choosing an ETF, you can take advantage of the industry's growth without depending solely on the performance of one startup.

What signals indicate a hydrogen project is likely to reach Final Investment Decision (FID)?

A hydrogen project is more likely to reach Final Investment Decision (FID) when it proves to be economically sound, incorporates careful planning to minimize risks, and secures reliable offtake agreements. Success also hinges on completing feasibility studies and obtaining the necessary approvals. On a global scale, more than 4 million metric tons per year of low-carbon hydrogen capacity have already achieved FID, highlighting significant progress in this rapidly advancing sector.

How can I tell if hydrogen tax credits and subsidies will last long enough to matter?

To gauge how long hydrogen tax credits and subsidies might stick around, keep an eye on updates from the Treasury and IRS. These agencies set the rules for which projects qualify. Recent regulations indicate ongoing backing, but possible adjustments - like tighter hourly matching rules - could impact whether projects remain practical and attract investment. Experts suggest closely following these regulatory changes to better understand the future stability of these incentives.