Hydrogen Power Costs: Green vs. Blue Hydrogen

Hydrogen production is rapidly evolving as a key player in reducing carbon emissions, but the way it's made greatly impacts both its cost and environmental footprint. Here's the quick takeaway:

- Green hydrogen: Produced using renewable energy to split water. Costs range from $3.50–$6.00/kg in 2026. Prices depend heavily on renewable electricity and electrolyzer technology.

- Blue hydrogen: Made from natural gas with carbon capture. Costs are lower at $2.00–$3.50/kg, but methane leaks and incomplete CO₂ capture still contribute emissions.

Key Insights:

- Cost Trends: Green hydrogen is closing the cost gap with blue hydrogen faster than expected. By 2030, green hydrogen could be cheaper in many regions.

- Driving Factors: Renewable energy prices and advancements in electrolyzers are making green hydrogen more affordable. Blue hydrogen relies on natural gas prices and carbon capture efficiency.

- Policy Impact: U.S. tax credits like the Inflation Reduction Act's $3.00/kg subsidy for green hydrogen and carbon pricing over $100/ton CO₂ are reshaping the market.

- Future Outlook: Blue hydrogen may remain viable short-term, but green hydrogen is expected to dominate by 2035 due to lower emissions and improving economics.

Bottom Line: If you're investing in hydrogen, green hydrogen offers long-term potential, while blue hydrogen is a transitional option in regions with cheap natural gas and effective carbon capture.

Grey vs. blue vs. green hydrogen | The Future of Energy [simplified]

sbb-itb-501186b

Green Hydrogen Production Costs

The cost of producing green hydrogen largely depends on electricity prices and the expenses associated with electrolyzers. As of 2026, renewable electricity remains the most significant factor in the overall cost. Prices can vary widely based on whether grid power, solar arrays, or wind farms are used. For example, grid electricity priced at $0.05/kWh results in hydrogen costs of $4.37 to $5.13 per kg, while a grid price of $0.07/kWh increases costs to $5.50 to $6.27 per kg.

Electricity and Renewable Energy Prices

The type of renewable energy used plays a big role in determining costs. Interestingly, lower electricity prices don’t always translate to cheaper hydrogen because of the impact of capacity factors. For instance, utility-scale solar PV in Los Angeles is priced competitively at $0.029–$0.032/kWh. However, its 31.8% capacity factor leads to higher hydrogen costs - around $5.54–$6.09 per kg. On the other hand, Class 1 onshore wind, with a slightly lower electricity price of $0.028/kWh but a much higher capacity factor of 52.1%, produces hydrogen at approximately $4.22 per kg. The limited operational hours of solar panels drive up costs per kilogram compared to wind farms.

For facilities needing continuous hydrogen production, combining solar PV with battery storage and grid connections could help. This approach might achieve costs as low as $2.02 per kg in Texas and $2.18 per kg in California within the next decade. However, designing systems for hourly reliability instead of annual averages can increase costs by 35% to 106%, due to the need for larger solar installations and extensive storage capacity.

Electrolyzer Technology Improvements

Electricity costs aren’t the only factor; advancements in electrolyzer technology also play a crucial role in lowering prices. Currently, PEM electrolyzers cost between $1,000 and $1,500 per kW, but this is expected to drop below $400 per kW in the next 10 to 15 years. This reduction will come from innovations in materials, scaling production, and standardizing designs .

"Electricity consumption is the largest factor in the cost of hydrogen produced by electrolysis. Higher electrolyzer efficiency reduces electricity consumption and lowers the cost of hydrogen produced." - Tony Leo, Retired Executive, FuelCell Energy

Efficiency improvements are also critical. For example, Solid Oxide Electrolyzer Cells (SOECs) can achieve efficiencies of 90–100%, significantly cutting electricity use from 55 kWh/kg closer to hydrogen’s energy content of 33 kWh/kg . Additionally, SOECs avoid using costly noble metals like platinum and iridium, helping to manage costs as production scales up.

These advancements are shaping the present and future of green hydrogen pricing.

Current and Future Green Hydrogen Prices

Considering the interplay of electricity and equipment costs, today’s green hydrogen prices in the U.S. range between $4.00 and $6.00 per kg for PEM-based production. Broader industry estimates place the range at $2.50 to $6.80 per kg, depending on factors like location and electricity source. The U.S. Department of Energy’s "Hydrogen Shot" initiative aims to reduce these costs significantly, targeting $2.00 per kg by 2025 and an ambitious $1.00 per kg by 2030. In regions where renewable electricity costs $20 per MWh or less, prices could fall below $2.50 per kg in the near future and potentially drop under $1.00 per kg by 2040, provided innovation and deployment continue at a rapid pace.

These cost trends are critical for professionals planning future infrastructure. The current gap between today’s prices and 2030 goals presents both challenges and opportunities for designing systems that remain viable over decades.

Blue Hydrogen Production Costs

Blue hydrogen production relies on steam methane reforming (SMR) combined with carbon capture and storage (CCS). Unlike green hydrogen, which depends heavily on renewable electricity costs, blue hydrogen’s pricing is primarily influenced by natural gas markets. This creates unique economic challenges for facilities planning to produce hydrogen in 2026.

Natural Gas Price Effects

Natural gas is a major factor in the levelized cost of hydrogen (LCOH) for blue hydrogen, accounting for 50% to 65.9% of total production costs. This makes blue hydrogen highly sensitive to shifts in natural gas prices. From 2017 to 2022, U.S. natural gas prices ranged between $1.9/GJ and $6.1/GJ. In 2025, industrial prices began at $5.84 per thousand cubic feet (kcf) in January but dropped to $4.21/kcf by September.

These price fluctuations have a direct impact on production costs. For example, when natural gas costs $4.2/GJ, the baseline LCOH is approximately $1.64 per kg. If prices drop to $2.4/GJ, production costs can fall below $1.00 per kg when tax credits are applied. On the other hand, higher gas prices reduce blue hydrogen’s cost competitiveness, especially in high-cost regions like the European Union.

Carbon Capture and Storage Requirements

Adding CCS to a standard SMR process increases the LCOH by over 50% compared to gray hydrogen production without carbon capture. The CCS system itself adds 20% to 50% to the facility’s total capital costs [14,15]. For a 100 MW plant, capital expenditures typically range from $700 to $1,000 per kW, with operating costs between $0.05 and $0.09 per kg of hydrogen produced.

The cost to avoid CO₂ emissions for blue hydrogen is estimated at around $65 per metric ton of CO₂. Capture efficiencies usually range from 85% to 90%, though newer autothermal reforming (ATR) technologies aim for rates above 93% [1,15]. Locating facilities near saline reservoirs for CO₂ storage can reduce transport and storage costs. Additionally, the U.S. Inflation Reduction Act’s Section 45Q tax credit - which provides $85 per metric ton of CO₂ stored in saline reservoirs - can lower the LCOH by about 22.2%.

"The addition of CCS for low-carbon hydrogen increases the levelized cost by more than 50% for the reforming production." – Nature Communications

These factors are critical in shaping both current and future pricing strategies.

Current and Future Blue Hydrogen Prices

By 2026, blue hydrogen production costs in the U.S. are expected to range from $1.80 to $4.70 per kg, depending on natural gas prices and CCS efficiency. Industry estimates generally place costs between $2.50 and $3.50 per kg without substantial subsidies [14,15]. This makes blue hydrogen more affordable than green hydrogen, which typically costs between $3.50 and $6.00 per kg.

The Air Products SMR+CCS facility in Port Arthur, Texas, is one of the few large-scale blue hydrogen projects currently operating in the U.S. As of 2021, it produced 0.23 million metric tons of blue hydrogen annually, with captured CO₂ used in enhanced oil recovery. Globally, blue hydrogen capacity is projected to grow to 6 to 12 million metric tons per year by 2030. However, without incentives like the 45Q tax credit, blue hydrogen is unlikely to meet the Department of Energy’s "Hydrogen Shot" goal of $1.00 per kg by 2030.

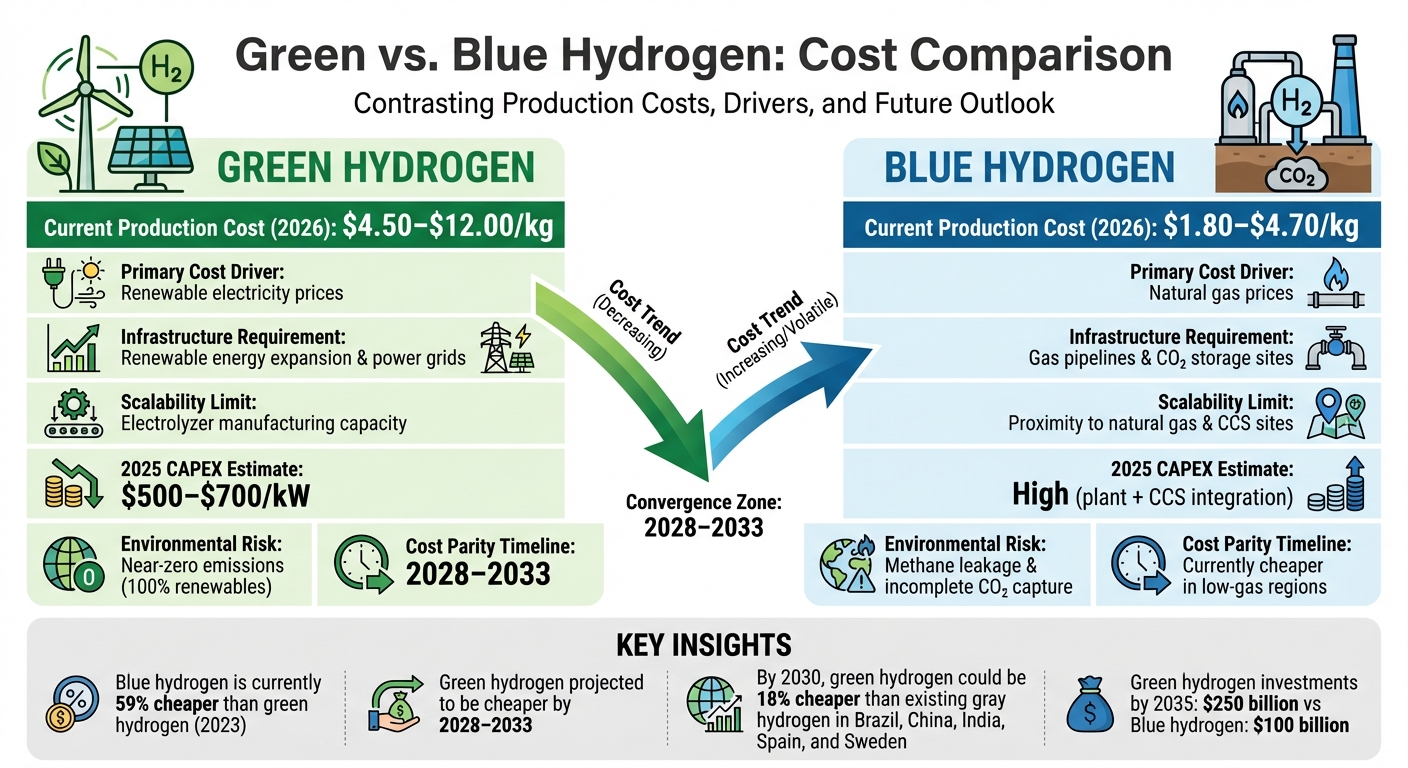

Green vs. Blue Hydrogen: Cost Comparison

Green vs Blue Hydrogen Production Costs Comparison 2026-2030

Let’s dive into the numbers and factors that set green hydrogen apart from blue hydrogen, focusing on current costs, future trends, and scalability challenges.

When Will Costs Reach Parity?

As of 2023, blue hydrogen is significantly cheaper - about 59% less expensive than green hydrogen. But this cost gap is narrowing faster than anticipated.

Projections show green hydrogen could overtake blue hydrogen in cost by 2028 when using Chinese alkaline electrolyzers. For Western systems, this shift is expected between 2030 and 2033, though variations in regional gas prices and CO₂ capture efficiencies may impact these timelines. According to Adithya Bhashyam, a hydrogen analyst at BloombergNEF:

"Using Western-made alkaline systems, green hydrogen beats out blue hydrogen by 2030 in all but a handful of modeled markets".

Blue hydrogen’s competitiveness depends heavily on natural gas prices and the efficiency of carbon capture. In regions where natural gas costs $1.50 or less per thousand cubic feet, blue hydrogen could remain a viable option until 2040 - but only if CO₂ capture rates exceed 90% and methane leakage stays below 1%. Conversely, in areas where gas prices hit $4.00 per thousand cubic feet, blue hydrogen may lose its cost advantage.

By 2030, green hydrogen from newly built plants is projected to be up to 18% cheaper than operating existing gray hydrogen facilities in countries like Brazil, China, India, Spain, and Sweden. Policy incentives are playing a big role in accelerating this transition.

Scalability and Infrastructure Needs

Scaling green hydrogen production depends on rapidly expanding renewable energy capacity and ramping up electrolyzer manufacturing. For costs to drop, production must shift from small-scale facilities producing around 10 MW annually to industrial-scale plants capable of generating 700 MW per year. While the technology is already proven, the pace of deployment will hinge on how quickly manufacturers can expand their production lines.

Blue hydrogen, on the other hand, faces constraints tied to geography and logistics. Facilities must be located near both natural gas sources and carbon capture and storage (CCS) sites. Additionally, the autothermal reforming (ATR) technology required for low-emission blue hydrogen is still in early stages of commercial deployment, with large prototypes existing but not yet widely scaled.

Grid-connected electrolyzers for green hydrogen benefit from proximity to consumers but come with higher electricity costs due to grid fees, which can add about $30 per MWh. Off-grid electrolyzers located at renewable energy sites avoid these fees but require significant investment in pipelines or alternative transport infrastructure for long-distance hydrogen delivery.

Transport and storage costs also differ. For green hydrogen, these expenses are estimated at $10 to $30 per MWh in 2025, potentially dropping to $5 to $15 per MWh by 2050 as infrastructure improves. Electrolyzer system capital costs are expected to decline from $500–$700 per kW in 2025 to $100–$300 per kW by 2050.

Cost Comparison Table

Here’s a breakdown of the key cost and scalability factors for green and blue hydrogen:

| Factor | Green Hydrogen | Blue Hydrogen |

|---|---|---|

| Current Production Cost | $4.50–$12.00/kg | $1.80–$4.70/kg |

| Primary Cost Driver | Renewable electricity prices | Natural gas prices |

| Infrastructure Requirement | Renewable energy expansion & power grids | Gas pipelines & CO₂ storage sites |

| Scalability Limit | Electrolyzer manufacturing capacity | Proximity to natural gas & CCS sites |

| Cost Parity Timeline | 2028–2033 (vs. new blue) | Currently cheaper in low-gas regions |

| Environmental Risk | Near-zero emissions (if powered by 100% renewables) | Methane leakage & incomplete CO₂ capture |

| 2025 CAPEX Estimate | $500–$700/kW | High (plant + CCS integration) |

While blue hydrogen holds a short-term cost edge in places like the U.S., green hydrogen is rapidly catching up. The decision between these options ultimately comes down to regional natural gas prices, access to renewable energy, and policy-driven incentives.

Policy and Market Effects

Technological progress alone isn’t enough to close the cost gap in hydrogen production - policy measures now play a crucial role. Government initiatives are rapidly reshaping the hydrogen market, influencing the economics of both green and blue hydrogen. The Inflation Reduction Act (IRA) of 2022 and the Bipartisan Infrastructure Law have allocated billions of dollars to advance clean hydrogen technologies.

Decarbonization Targets and Incentives

The Department of Energy (DOE) has set ambitious goals with its "Hydrogen Energy Earthshot", aiming to reduce hydrogen production costs to $1.00 per kilogram by 2031. This initiative is backed by $9.5 billion from the Bipartisan Infrastructure Law, including $7 billion earmarked for seven Regional Clean Hydrogen Hubs.

In October 2023, the DOE announced funding for these hubs, which will integrate hydrogen production, storage, and usage facilities. These hubs will utilize both renewable-powered electrolysis (green hydrogen) and natural gas with carbon capture (blue hydrogen). The National Clean Hydrogen Strategy outlines even bolder production goals: 10 million metric tons annually by 2030, scaling to 20 million metric tons by 2040 and reaching 50 million metric tons by 2050.

While these targets are driving adoption, sustained policy support will be essential through at least 2035. Without continued incentives, neither green nor blue hydrogen is likely to hit the $1.00/kg target independently. Blue hydrogen, in particular, faces significant hurdles:

"Without tax incentives, however, it is hard for blue hydrogen production to reach the cost target of $1/kg H2" - Nature Communications

These aggressive goals underscore the importance of robust tax incentives to lower production costs further.

Carbon Pricing and Tax Credits

Tax credits are a cornerstone of the hydrogen economy’s evolving financial models. The IRA provides two key incentives: Section 45V (Production Tax Credit) and Section 45Q (Carbon Sequestration Credit). However, facilities can only claim one of these credits.

- Section 45V offers tiered credits based on lifecycle emissions, ranging from $0.60 to $3.00 per kilogram of hydrogen. To qualify for even the minimum credit, production must emit less than 4.0 kg of CO₂ equivalent per kilogram. This poses challenges for blue hydrogen, as its median lifecycle emissions - estimated at 4.1 to 4.6 kg CO₂e per kilogram - often exceed this threshold unless significant methane abatement measures are implemented.

- Section 45Q, on the other hand, often provides better financial outcomes for blue hydrogen facilities. For example, blue hydrogen produced through steam methane reforming with carbon capture can see costs reduced by about 22.2% under the 45Q credit, compared to a 13.7% reduction under the lowest tier of the 45V credit.

Green hydrogen benefits more substantially from Section 45V, particularly at the highest tier. The IRA’s production tax credits effectively act as an implicit carbon price ranging from $100 to $350 per metric ton of CO₂. This level of support is vital because:

"Electricity-based production only achieves cost-competitiveness with fossil-based pathways if embodied emissions of electricity inputs are not counted under U.S. Tax Code Section 45V guidance" - Nature Communications

Carbon pricing is becoming another critical factor. Projections suggest that carbon pricing exceeding $100 per ton of CO₂ will make traditional gray hydrogen - which currently costs $1.50 to $2.50 per kilogram - uncompetitive by 2030. For blue hydrogen, if natural gas leakage surpasses 4%, the cost of mitigating residual emissions to achieve net-zero could add as much as $2.55 per kilogram. This highlights how blue hydrogen’s long-term viability depends heavily on effective upstream methane management.

Investors are showing strong confidence in green hydrogen’s potential. By 2035, green hydrogen investments are expected to reach $250 billion, compared to $100 billion for blue hydrogen. Policy incentives are clearly shifting the market, and the cost advantage of blue hydrogen is narrowing faster than many had anticipated.

Conclusion

What Professionals Need to Know

As the hydrogen market continues to evolve, professionals making investment decisions need to focus on key trends and factors shaping the industry. Right now, blue hydrogen has a 59% cost advantage over green hydrogen for projects financed in 2023. However, this gap is narrowing faster than previously predicted, with green hydrogen expected to become more affordable 1–3 years earlier than earlier forecasts suggested.

When deciding between green and blue hydrogen, consider three critical factors: regional gas prices, carbon pricing exposure, and regulatory timelines. Blue hydrogen remains a practical option in areas with low natural gas prices, especially when facilities can achieve CO₂ capture rates above 90% and methane leakage stays below 1%. On the other hand, in regions with high gas prices - like much of Europe - the economic case for blue hydrogen is already shrinking or has disappeared entirely.

Policy incentives are also a game-changer. For instance, the IRA's Section 45V tax credit offers up to $3.00 per kilogram, significantly boosting the prospects for green hydrogen. This kind of support is why projections show green hydrogen attracting $250 billion in investments by 2035, compared to $100 billion for blue hydrogen.

The bottom line? Blue hydrogen is best viewed as a short-term solution. For projects with operational timelines extending beyond 2035, green hydrogen is the safer bet, offering better protection against future carbon pricing and stricter emission regulations. Industry analysts agree that the cost advantage will shift to green hydrogen sooner than many expected.

Infrastructure is another critical piece of the puzzle. Reliable platforms like Electrical Trader ensure access to essential equipment - transformers, breakers, and high-voltage systems - needed for both green and blue hydrogen projects.

Finally, the Department of Energy’s ambitious target of $1.00 per kilogram by 2031 is within reach, provided policy support remains consistent through at least 2035. Long-term regulatory stability is essential to achieving this milestone and driving hydrogen's future as a clean energy solution.

FAQs

How do new electrolyzer technologies lower the cost of green hydrogen production?

Advances in electrolyzer technology are making green hydrogen more affordable by boosting efficiency, extending durability, and scaling up production capabilities. Researchers and engineers are working on streamlining designs, minimizing the use of rare or costly materials, and building larger electrolyzers to lower production costs.

These breakthroughs are cutting both equipment and operational expenses, with some experts predicting cost reductions of as much as 80% in the near future. As renewable electricity becomes cheaper, these technological strides are positioning green hydrogen as a more competitive option, speeding up its integration into the shifting energy landscape.

How do U.S. tax credits make green hydrogen more affordable and competitive?

U.S. tax credits, such as the §45X advanced manufacturing production tax credit, play a key role in lowering the cost of producing green hydrogen. These credits provide financial incentives to clean energy manufacturers, helping to make green hydrogen a more affordable and competitive option compared to blue hydrogen and traditional fossil fuels.

By supporting renewable energy technologies, these policies drive investment in cleaner hydrogen production and speed up the shift toward more sustainable energy solutions across the United States.

Why is blue hydrogen seen as a temporary solution compared to green hydrogen?

Blue hydrogen is sometimes considered a short-term fix because it’s produced using natural gas paired with carbon capture technology. While this method can cut emissions and offer a more affordable option in the near term, it still relies on fossil fuels. That means it’s tied to the price swings and environmental issues that come with them.

On the other hand, green hydrogen is created using renewable electricity and water, making it a cleaner and more sustainable option over time. With the cost of renewable energy dropping and advancements in electrolyzer technology, green hydrogen is poised to become more cost-effective and widely used. This aligns with global goals to shift toward cleaner, renewable energy solutions.