Middle East Power Equipment: 2025 Pricing Trends

The Middle East power equipment market in 2025 saw rising costs driven by material shortages, advanced technology integration, and large-scale infrastructure investments. Key highlights:

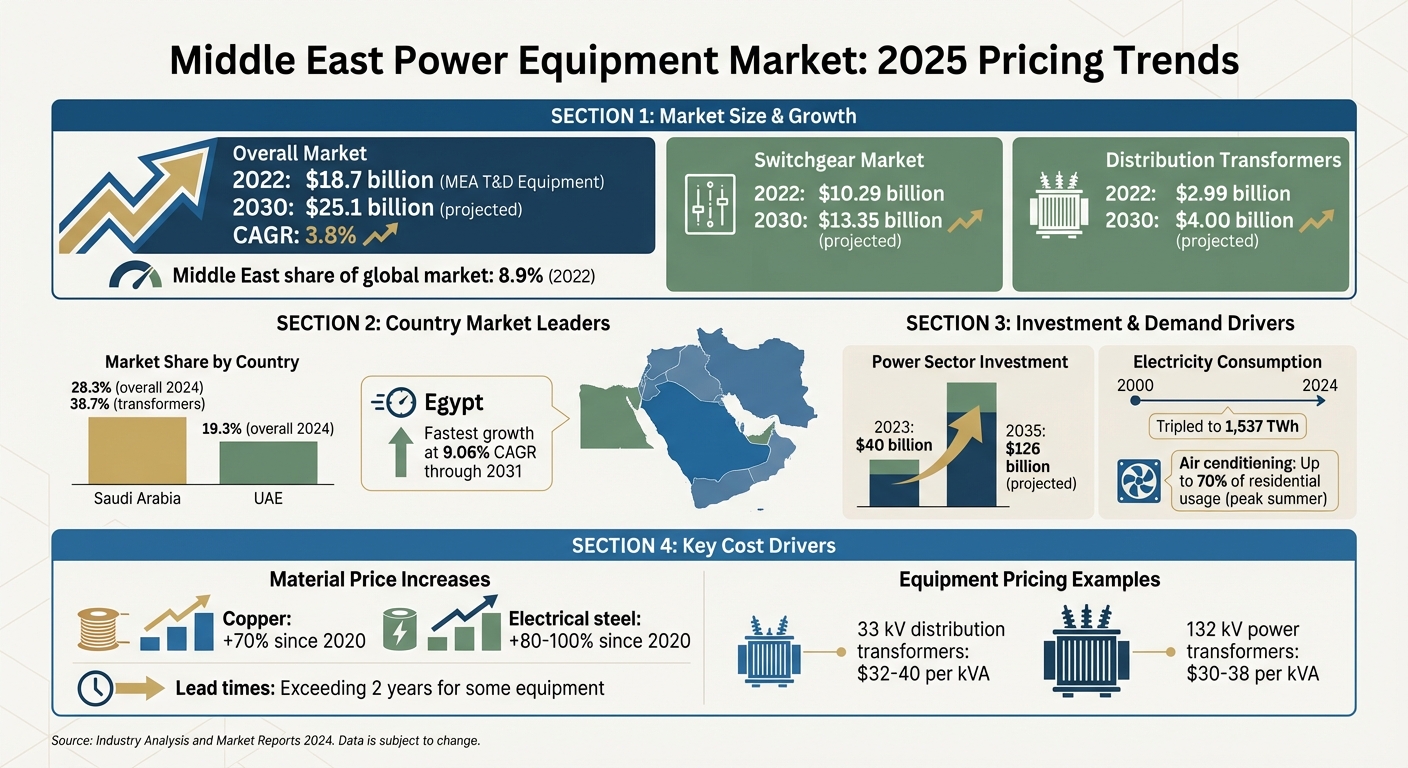

- Market Growth: The region’s power equipment market is expanding, with switchgear valued at $10.29 billion in 2022 and projected to reach $13.35 billion by 2030. Distribution transformers are expected to grow from $2.99 billion to $4.00 billion in the same period.

- Cost Drivers: Supply chain delays, copper and steel price surges, IoT-based systems, and harsh environmental conditions are inflating prices. Lead times for some equipment exceed two years.

- Country Insights: Saudi Arabia leads with a 38.7% share of the transformer market, spurred by Vision 2030 projects. The UAE focuses on smart grids, while Egypt faces unstable pricing due to currency fluctuations.

- Equipment Trends: High-voltage transformers remain costly, with copper prices up 70% since 2020. Renewable energy integration is increasing demand for advanced, efficient equipment.

- Infrastructure Impact: Mega-projects like Saudi Arabia’s NEOM and UAE’s data centers are driving demand for specialized equipment, pushing prices higher.

Long-term, prices will likely continue rising due to modernization efforts, renewable energy adoption, and increasing electricity demand.

Middle East Power Equipment Market Growth 2022-2030: Key Statistics and Projections

Middle East Power Equipment Market Overview

Market Size and Value

The Middle East power equipment market is growing quickly, carving out a significant role in the global electrical infrastructure industry. In 2022, the broader Middle East & Africa (MEA) electric power transmission and distribution (T&D) equipment market was valued at $18.7 billion, with projections indicating it could reach $25.1 billion by 2030, representing a 3.8% compound annual growth rate (CAGR). Within this, the Middle East alone accounted for 8.9% of the global market in 2022.

Breaking it down further, the switchgear market stood at $10.29 billion in 2022 and is anticipated to climb to $13.35 billion by 2030. Similarly, the distribution transformer segment grew from $2.99 billion in 2022 to an estimated $4.00 billion by 2030.

This expansion is fueled by surging electricity demand. Between 2000 and 2024, electricity consumption in the Middle East tripled, reaching 1,537 TWh. Extreme climatic conditions play a significant role, with air conditioning accounting for as much as 70% of residential electricity usage during peak summer months. The International Energy Agency has identified the Middle East as the third-largest driver of global electricity demand growth, trailing only China and India. Additionally, annual investments in the power sector are expected to increase from $40 billion in 2023 to approximately $126 billion by 2035. This influx of capital underscores the region's commitment to developing its power infrastructure.

These numbers paint a clear picture of the opportunities and players shaping the market's future.

Leading Countries and Market Players

Saudi Arabia and the United Arab Emirates (UAE) dominate the Middle East power equipment market, accounting for nearly half of the region's share. In 2024, Saudi Arabia led the pack with a 28.3% market share, while the UAE followed with 19.3%. Saudi Arabia also claimed a commanding 38.7% share of the distribution transformer market in 2022, bolstered by ambitious projects under Vision 2030 and major industrial contracts with companies like Saudi Aramco.

The market features a mix of global giants and regional manufacturers. Companies such as Hitachi Energy, Siemens, Schneider Electric, ABB, and GE Vernova captured over 50% of high-end power equipment tenders in 2025. These firms are at the forefront of advancing technologies like digital twins and IoT-based monitoring systems for extra-high-voltage and HVDC systems. On the regional front, manufacturers like alfanar Group, Bawan Co., WESCOSA, and Saudi Transformer Co. dominate in distribution-level equipment and sub-132 kV segments, leveraging local production requirements.

Key utilities and state-owned entities drive demand in the sector. Organizations such as the Saudi Electricity Company (SEC), Dubai Electricity and Water Authority (DEWA), and Saudi Aramco are pivotal, awarding contracts worth millions that shape supply chains across the region. For instance, in August 2025, DEWA commissioned four 132 kV substations with a combined capacity of 450 MVA, costing AED 725 million ($197 million). This was part of a larger AED 7.6 billion transmission project. Such large-scale investments highlight the scale and momentum of the power equipment market in the Middle East.

sbb-itb-501186b

2025 Pricing Factors and Cost Drivers

Supply Chain Issues and Material Costs

The challenges in global supply chains continue to escalate in 2025, significantly impacting costs. Shortages in key components like transformers, cables, and turbines have pushed lead times beyond two years. This is largely due to backlogs and the limited manufacturing capacity worldwide.

"These constraints are structural, not temporary and require strategic responses to secure supply",

warned PwC Middle East.

Adding to the strain, raw material bottlenecks are creating further issues. The demand for copper, rare earths, lithium, and polysilicon has outpaced global production, driving up prices. The push for smart grid technologies is also increasing equipment costs. Delays caused by interface risks are now commonplace, leading to project cost overruns.

| Equipment Category | Key Cost Driver | Impact on Pricing/Supply |

|---|---|---|

| Transformers & Cables | Global manufacturing capacity | Lead times exceeding 2 years |

| Switchgear | Smart functionality | Higher capital costs |

| Renewable Components | Raw materials (Lithium, Polysilicon) | Demand outstripping supply |

| Grid Infrastructure | Modernization & interconnections | Nearly 40% of power sector investment |

These material and production challenges are setting the stage for unpredictable pricing, further influenced by broader economic conditions.

Currency Exchange Rates and Economic Conditions

Economic trends in 2025 have created a two-tier pricing landscape. Countries that are net energy importers, such as Egypt, Lebanon, Morocco, and Tunisia, are grappling with heightened global price volatility, which complicates funding for essential upgrades. Meanwhile, oil and gas producers have found more stability, using revenue from hydrocarbon exports to invest in renewable energy projects and infrastructure.

To combat currency pressures and reduce reliance on imports, governments are reforming subsidies and encouraging local production. For example, in August 2025, Saudi Electricity Company awarded a $376 million contract to Saudi Power Transformers Co. to supply transformers for major projects like NEOM and the Red Sea development, aligning with national goals to localize production.

These economic dynamics are closely tied to regulatory changes, which also influence equipment costs.

Government Regulations and Trade Tariffs

In line with the global push for localization, new regulations now require 30%–50% local input for major projects. This has prompted international suppliers to set up regional facilities, increasing upfront costs but potentially stabilizing prices over time. A notable example is the joint venture between Voltamp Energy and Al Sharif Holding to establish a high-voltage transformer manufacturing facility in Saudi Arabia, with plans to produce 132kV units by 2025 and 380kV units by 2027.

Trade tariffs imposed by the U.S. have added financial strain to the GCC region, creating a more polarized economic climate. Additionally, regulatory processes for certifying equipment and connecting to the grid often take 6–12 months, which can delay projects and inflate costs. Specialized equipment for renewable energy - like solar inverters and grid stabilization systems - commands premium prices due to limited supplier competition and the unique demands of the region’s harsh conditions.

"Improving air conditioner efficiency standards could reduce peak demand growth by 35 GW by 2035 - equivalent to the total power generation capacity of Iraq today",

observed the IEA.

Country-by-Country Price Differences

Price Comparison by Country

When it comes to power equipment costs, regional differences across the Middle East are shaped by factors like infrastructure goals, import reliance, and economic conditions. Saudi Arabia stands out with the largest market revenue in transformers and high-voltage switchgear. This is largely due to the ambitious Vision 2030 projects, which have kept prices high but relatively stable.

The UAE, known for its quick adoption of IoT-enabled smart grids, faces higher costs for advanced equipment. However, its role as a major trading hub for global brands like Siemens and ABB helps offset some of the import-related price hikes. Meanwhile, Egypt experiences the region's most unstable pricing, driven by currency fluctuations and what industry experts describe as a "currency crunch." Despite this, Egypt has the fastest growth rate in the region - 9.06% CAGR through 2031 - thanks to projects like the 3 GW Egypt–Saudi interconnector, which was nearly completed by 2025.

| Country | Market Share/Position | Key Price Influencer | Growth Rate |

|---|---|---|---|

| Saudi Arabia | 38.7% (transformers), 25.89% (HV switchgear) | Vision 2030 megaprojects; local manufacturing | Steady expansion |

| UAE | Technology adoption leader | Advanced tech premiums; major trading hub | Moderate growth |

| Egypt | Fastest-growing market | Currency volatility; grey market competition | 9.06% CAGR through 2031 |

| Qatar | Niche industrial focus | North Field LNG expansion; FIFA legacy projects | Modest growth |

In Qatar, costs are primarily driven by specialized industrial projects, especially those tied to the North Field East LNG expansion. In contrast, Egypt faces challenges from a thriving grey market, which undercuts original equipment manufacturer (OEM) pricing by 15–20% for sub-132 kV equipment. This creates a dual pricing structure that often compromises quality and reliability. These variations highlight how local factors influence pricing strategies across the region.

"Saudi Arabia retained 25.89% of 2025 revenue as Vision 2030 accelerated substation rollout, while Egypt delivered the region's fastest switchgear growth", according to Mordor Intelligence.

Coastal nations like Saudi Arabia, the UAE, and Qatar benefit from easier access to raw materials and shorter supply chains, reducing transportation costs compared to landlocked regions. However, all countries in the region face higher prices for equipment designed to handle extreme conditions, such as temperatures reaching 122°F (50°C), sandstorms, and corrosive marine environments. These challenges, combined with regulatory and material costs, contribute to the elevated pricing discussed earlier.

Pricing Trends by Equipment Type

Low-Voltage Equipment

The low-voltage switchgear market in the Middle East and Africa reached $2.30 billion in 2025, with a projected growth rate of 5% CAGR through 2030. Price increases in 2025 were driven by fluctuating raw material costs, supply chain disruptions, and trade tariffs. To counteract these challenges, major manufacturers like Stanley Black & Decker raised prices during the second and third quarters of the year.

In the power tools segment, fierce competition among over 50 key players caused average selling prices to drop by about 10%. The regional power tools market was valued at approximately $1.5 billion in 2025. Infrastructure projects, including Saudi Arabia's NEOM, and regulatory updates like the Saudi Building Code SBC 601/602, boosted demand for energy-efficient, higher-priced equipment. Construction accounted for over 25% of the market share, while the rapid growth of data centers in Oman, Saudi Arabia, and the UAE spurred demand for specialized low-voltage distribution equipment.

This pricing landscape stands in contrast to the transformer market, where material shortages and supply-demand mismatches pose ongoing challenges.

Transformers and High-Voltage Equipment

Transformer prices remained high in 2025 due to a global supply-demand imbalance. While demand grew by 7–9%, supply capacity only increased by 3–4%. The Middle East and Africa transformer market was valued at $5.37 billion in 2025, with Saudi Arabia accounting for 18.15% of the regional market. Lead times for some specialized large power-class transformers stretched up to three years.

Material costs significantly impacted transformer pricing. Copper and grain-oriented silicon steel, which together make up more than 50% of a transformer's material costs, saw sharp price increases - copper prices surged over 70%, and electrical steel costs rose by 80–100% since 2020. In the region, average prices for 33 kV distribution transformers ranged from $32–40 per kVA, while 132 kV power transformers were priced between $30–38 per kVA. Oil-cooled transformers dominated the market with an 83.95% revenue share, though air-cooled units are gaining traction with a 4.92% CAGR, driven by their adoption in hyperscale data centers and urban areas with strict fire-safety codes.

In August 2025, Saudi Electricity Company awarded a $376 million contract to Saudi Power Transformers Co. for the supply of distribution transformers to support the NEOM and Red Sea megaprojects. Additionally, Voltamp Energy and Al Sharif Holding formed a partnership to establish a high-voltage transformer plant in Saudi Arabia. The facility aims to produce 132 kV transformers by 2025 and 380 kV units by 2027, reducing reliance on imports.

Turning to power generation equipment, contrasting cost trends are evident between conventional systems and renewable energy technologies.

Power Generation Equipment

Pricing trends in power generation equipment during 2025 revealed a divide. Traditional systems, especially those incorporating advanced IoT-based control features, saw rising costs. Meanwhile, renewable energy technologies, particularly solar and wind, experienced cost declines, increasing their competitiveness against conventional gas-fired systems.

"With limited gas supplies and falling renewable technology costs, nearly all MENA countries are actively procuring or planning solar and wind projects." – MEED

In the stationary Battery Energy Storage System (BESS) market, there has been a shift from nickel manganese cobalt (NMC) to lithium iron phosphate (LFP) chemistries. This transition aims to better control costs in utility-scale systems. Furthermore, in December 2022, Saudi Electricity Co. signed $720 million worth of contracts with Chinese and Saudi companies to implement a smart grid project for the Kingdom's electricity distribution network.

How Infrastructure Projects Affect Pricing

Major Projects Driving Equipment Demand

Infrastructure projects are playing a critical role in shaping equipment prices, largely due to skyrocketing demand. Investments in infrastructure are projected to rise sharply, from $40 billion in 2023 to over $126 billion by 2035, significantly impacting equipment costs. A substantial portion of this funding is being allocated to grid upgrades and energy storage developments.

Saudi Arabia stands out as a leader in this infrastructure surge. The country plans to boost its high-voltage transmission capacity by nearly 200,000 MVAs, supported by the construction of around 560 new substations. One notable initiative is the "Saudi Voltamp" joint venture between Oman’s Voltamp Energy Company and Saudi Arabia’s Al Sharif Holding Group. Starting in 2025, this $10 million project will produce 132 kV high-voltage transformers, aiming for an annual capacity of 30,000 MVA, with plans to expand to 380 kV transformers by 2027. These efforts are expected to not only enhance local production but also help stabilize equipment prices.

The UAE is also fueling equipment demand with ambitious projects. For example, in May 2025, G42, a UAE-based telecommunications firm, announced plans for a 5 GW data center campus. Around the same time, Saudi AI company HUMAIN, backed by the Public Investment Fund, unveiled projects totaling 1 GW. These developments are driving demand for specialized power distribution and cooling systems. Additionally, Abu Dhabi has greenlit 144 new infrastructure projects with a combined budget of nearly $18 billion. Collectively, these projects highlight the region’s focus on high-tech, value-driven infrastructure, setting the stage for further advancements in renewable energy integration.

Renewable energy projects are also pushing up prices for specialized equipment. For instance, in December 2021, a consortium led by Hitachi Energy secured a contract from the Saudi Electricity Company and the Egyptian Electricity Transmission Company to implement an HVDC interconnection project. This initiative will allow the transfer of up to 3,000 MW of electricity between Saudi Arabia and Egypt, creating a surge in demand for high-voltage transmission equipment.

By 2030, the region is expected to add over 600,000 MVAs in transmission capacity, with renewable-focused equipment growing at an annual rate of 15%.

These large-scale projects are also accelerating the adoption of smart grid technologies. For example, Siemens AG was awarded a contract in December 2022 by Egypt’s North Delta Electricity Distribution Company to build a medium-voltage ADMS control center and a smart metering system for the Damietta region. The shift toward digital monitoring and automated distribution systems is driving demand for advanced two-way communication equipment, often at premium prices.

Price Forecasts and Market Outlook Through 2030

New Technologies and Their Effect on Costs

The modernization of smart grids is reshaping equipment pricing across the Middle East. For instance, advanced distribution transformers equipped with IoT-based real-time monitoring are now priced at a premium, which has also pushed up the costs of switchgear due to their enhanced functionality.

Take gas-insulated switchgear (GIS) as an example. While GIS units come with higher upfront costs, they offer significant savings over time thanks to their compact designs and lower environmental impact. With a projected 3.5% CAGR, GIS is expected to be the fastest-growing insulation segment through 2030, especially in urban areas where space is limited.

The shift toward renewable energy is another major factor. The demand for specialized equipment, such as bi-directional transformers, is rising to accommodate variable inputs from solar and wind installations. Shell core transformers, which boast efficiencies of 98% to 99%, accounted for 32.4% of the market share in 2024. These high-efficiency transformers, though more costly than traditional options, are becoming essential for modernizing grids. These technological advancements are expected to drive steady price increases in the market over the next decade.

Long-Term Development and Price Trends

Beyond technological shifts, market forecasts indicate that equipment prices will continue to rise through 2030. The Middle East switchgear market, for example, is expected to grow from $10.58 billion in 2023 to $13.35 billion by 2030, reflecting a 3.4% CAGR. Distribution transformers are set to see even more robust growth, with projections showing an increase from $1.8 billion in 2024 to $3.5 billion by 2034, achieving a 6.8% CAGR.

Low-voltage switchgear, which led the market with a 44.3% share in 2022, is anticipated to maintain the highest growth rate at 3.9% through 2030. This growth is fueled by booming residential and commercial construction, particularly in Saudi Arabia and the UAE.

Investment in the power sector further underscores these trends. Total spending reached $44 billion in 2024 and is expected to increase by 50% by 2035. Nearly 40% of this investment will go toward upgrading grid infrastructure to reduce transmission losses and enhance regional interconnections. With electricity demand forecasted to rise by 50% by 2035, prices for advanced, renewable-compatible systems are likely to remain elevated through the decade.

PTR Perspective Episode 13: HV Switchgear in the Middle East - Demand Drivers and SF6 Alternatives

Conclusion

Making informed decisions in procurement starts with a solid grasp of Middle East power equipment pricing. By 2030, the switchgear market is expected to hit $13.35 billion, while the distribution transformer market is projected to reach $4.0 billion, fueled by the integration of smart grids and the growing demand for advanced technologies. These developments are shaped by notable regional differences.

For instance, Saudi Arabia commands a 38.7% share of the distribution transformer market, while Egypt is emerging as a leader in high-voltage switchgear, boasting an impressive CAGR of over 9% through 2031. Factors like currency fluctuations, supply chain hurdles, and varying regulations further complicate procurement strategies in the region.

Although the initial costs of high-efficiency equipment can be steep, the long-term savings and compliance with updated standards make them worthwhile investments. Nearly 40% of power sector spending is now directed toward grid modernization, emphasizing infrastructure upgrades. Navigating this dynamic landscape requires procurement teams to carefully balance immediate budget constraints with forward-looking investments that ensure competitiveness.

Electrical Trader simplifies this process by offering a platform where professionals can access verified listings for electrical equipment. Whether you're looking for new, used, or surplus components, the marketplace connects you with trusted manufacturers like Siemens, ABB, and GE. With advanced technical filtering tools, it helps alleviate supply chain challenges and keeps projects on track.

FAQs

What is causing power equipment prices to rise in the Middle East?

The rising cost of power equipment in the Middle East can be traced to several key factors. One major driver is the disruption in global supply chains and shortages of critical materials like steel and copper - both essential for producing electrical components. These supply issues have pushed up raw material prices, directly impacting manufacturing costs.

At the same time, the region's large-scale infrastructure projects, including efforts to expand power grids and shift toward renewable energy, have fueled demand for equipment such as transformers and switchgears. This heightened demand has added further strain to supply chains, contributing to price increases.

Regional policies also play a role. For instance, tariffs on imported raw materials aim to promote local manufacturing but often lead to higher costs for components. On top of that, logistical challenges and procurement delays - particularly in key markets like Saudi Arabia and Egypt - add to the overall expense. Together, these factors are driving the upward trend in power equipment prices across the Middle East.

How do economic conditions in different Middle Eastern countries affect power equipment prices?

Economic factors across Middle Eastern nations significantly shape the pricing of power equipment by affecting supply chains, material costs, and market demand. For instance, when infrastructure projects expand rapidly or populations grow, the demand for essential equipment like transformers and switchgears can spike. This often results in higher prices, especially in regions where local manufacturing capacity is limited. Additionally, the fluctuating costs of materials like steel and copper - often influenced by global supply chain disruptions or tariffs - play a major role in determining equipment prices.

Government policies and financial stability also weigh heavily on these costs. In countries with robust financial systems or access to substantial investment resources, large-scale energy projects are often supported, which can help stabilize pricing. Conversely, regions facing political or economic instability tend to see increased risks, which can drive up the costs of both materials and equipment. Ultimately, pricing trends for power equipment in the Middle East are shaped by a mix of local economic conditions, resource availability, and policy choices.

How do large infrastructure projects influence the power equipment market in the Middle East?

Large infrastructure projects play a major role in driving the power equipment market across the Middle East. With growing populations, rapid industrialization, and a push toward cleaner energy, these projects often demand extensive upgrades and expansions of existing power grids.

The surge in renewable energy investments - particularly in solar and wind power - has significantly increased the need for equipment such as transformers, switchgear, and advanced grid systems. Regional investments in electrical infrastructure are projected to reach around $175 billion by 2024, highlighting the shift toward modern and sustainable energy solutions. This momentum is also fueling the adoption of cutting-edge technologies like smart transformers and advanced protection systems, which are critical for creating power networks that are both resilient and efficient.