Latin America Power Distribution Market Trends 2026

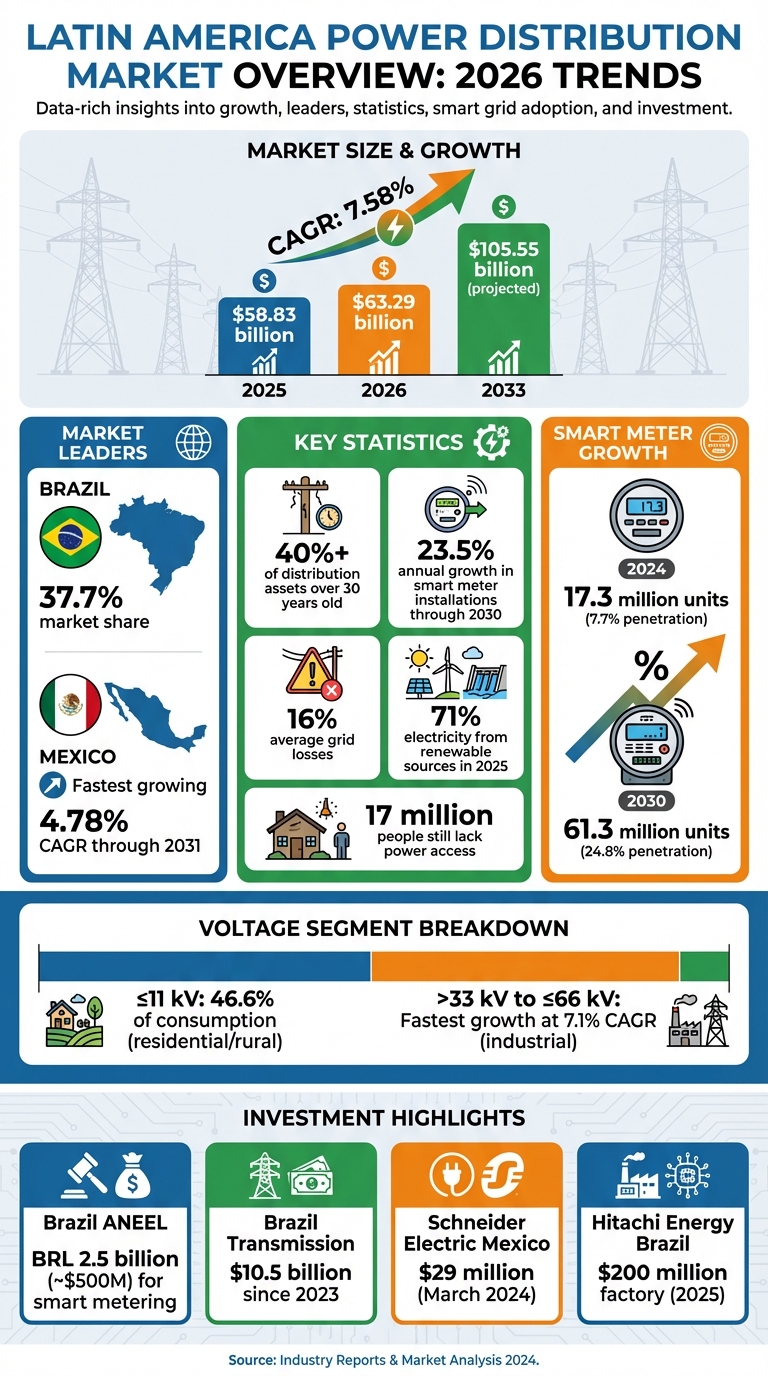

The Latin American power distribution market is evolving quickly in 2026, driven by urban growth, industrial demand, and the need to replace aging infrastructure. The market grew to $58.83 billion in 2025 and is projected to reach $63.29 billion in 2026, with a 7.58% annual growth rate expected through 2033. Key trends include:

- Aging Infrastructure: Over 40% of distribution assets are over 30 years old, pushing for upgrades.

- Smart Grid Adoption: Demand for digital equipment like smart meters and automated systems is rising, with smart meter installations expected to grow by 23.5% annually through 2030.

- Urbanization and Industrial Growth: Cities like São Paulo and Mexico's industrial hubs are driving demand for reliable, modern grids.

- Renewable Energy Integration: Solar, wind, and battery storage projects are expanding, requiring advanced grid technologies.

Brazil leads the region with 37.7% of the market, while Mexico is seeing rapid growth due to near-shoring and EV infrastructure. Challenges include high grid losses (16%) and rural electrification gaps, but decentralized solutions like microgrids are helping underserved areas.

The push for modernization and renewable energy integration is reshaping Latin America's energy landscape, with opportunities in advanced equipment and digital solutions.

Latin America Power Distribution Market Growth 2025-2033

Market Size and Growth Projections for 2026

Financial Metrics and Market Forecasts

The Latin American power distribution component market is showing steady growth. Recent estimates put the market value at USD 58.83 billion in 2025, with projections to reach USD 63.29 billion in 2026. By 2033, this market is expected to nearly double, climbing to USD 105.55 billion, driven by a compound annual growth rate (CAGR) of 7.58%.

Focusing on specific segments, the transformer market stood at USD 4.79 billion in 2025 and is expected to grow modestly to USD 4.96 billion in 2026, eventually reaching USD 5.88 billion by 2031 at a CAGR of 3.47%. Meanwhile, the broader transmission and distribution market is set to expand from USD 10.37 billion in 2024 to USD 11.87 billion in 2026, and further to USD 19.04 billion by 2033, reflecting a 7% CAGR.

This upward trend underscores the pressing need to upgrade aging infrastructure. For instance, Mexico's Federal Electricity Commission (CFE) has flagged 25,000 kilometers (about 15,500 miles) of deteriorating lines that require immediate replacement. High-efficiency transformers are critical to this effort, addressing both current challenges and future energy demands.

Market Breakdown by Voltage Levels

Delving deeper into the market, the ≤ 11 kV segment leads the way, representing 46.6% of total consumption in 2024. This dominance is attributed to the fact that over 75% of electricity distribution occurs at these lower voltages, primarily serving residential areas and rural networks.

At the same time, the >33 kV to ≤66 kV category is experiencing the fastest growth, with a CAGR of approximately 7.1%. This surge is fueled by energy-intensive industries such as copper mining in Peru and offshore oil operations in Brazil. Additionally, Mexico's push for industrial near-shoring and the expansion of EV charging corridors is driving demand for medium-voltage equipment to support manufacturing and infrastructure development.

The transition toward higher voltage systems reflects a broader industry shift. Utilities are prioritizing infrastructure capable of not only meeting today’s energy demands but also accommodating future needs, such as industrial automation, renewable energy integration, and the growing trend of electrification. These developments align with the modernization and capacity expansion efforts outlined earlier.

sbb-itb-501186b

Main Demand Drivers in the Region

Urbanization and Industrial Growth

The rapid pace of urbanization in Latin America is putting immense pressure on power networks in major metropolitan areas. Cities like São Paulo, Bogotá, and Lima are seeing significant infrastructure upgrades to keep up with growing populations. Between 2020 and 2023, Brazil alone added over 15 million new residential connections, leading to widespread upgrades in equipment like transformers, switchgear, and low-voltage systems in densely populated neighborhoods.

Industrial growth is another major factor. Mexico's near-shoring boom - where manufacturers move operations closer to the U.S. - has created a surge in demand for dependable electrical systems. For instance, in March 2024, Schneider Electric invested $29 million to upgrade power systems in Mexican industrial parks. This investment specifically addressed voltage fluctuation issues caused by the rapid influx of manufacturing facilities, ensuring grid stability for new production lines. Similarly, Toyota utilized WEG dry-type transformers at its 4.3 million–square–foot Sorocaba campus in Brazil to safeguard sensitive robotics in its paint shops from power inconsistencies, highlighting the need for precise voltage regulation in advanced manufacturing setups.

In Chile and Peru, mining operations are expanding into remote and challenging areas. Copper extraction sites now require robust infrastructure like 66 kV substations and medium-voltage switchgear to handle heavy loads in harsh environments, pushing distribution networks beyond urban centers. Additionally, the rise of hyperscale data centers in cities such as São Paulo, Querétaro, and Santiago has created a surge in demand for medium-capacity transformers (10 to 100 MVA). These accounted for 73.66% of the market share in 2025, underscoring the growing role of digital infrastructure in shaping regional power strategies.

These shifts in urbanization and industrial activity are prompting a reassessment of grid capacity and efficiency across the region.

Electricity Consumption and Network Expansion

The rise in electricity consumption is another critical factor driving upgrades in power distribution networks. In 2023, regional electricity consumption grew by 4.7% year-over-year. This increase not only reflects higher demand but also reveals deeper changes in how energy is produced, distributed, and consumed across Latin America. However, aging infrastructure continues to cause inefficiencies, outages, and energy losses, creating a pressing need for modernization.

To meet this rising demand, utilities are expanding grids with systems designed to handle bidirectional power flows, rapid load changes, and renewable energy integration. For example, Brazil's "Recharge Brazil" initiative aims to install 120,000 public and private EV charging stations by 2027. Each station requires specialized transformers and smart meters to manage charging cycles and maintain grid stability. In September 2024, WEG Industries announced a R$543 million investment (about $108 million) to expand transformer production in Minas Gerais and Rio Grande do Sul to address growing domestic demand.

These efforts illustrate the region's focus on modernizing and expanding its power infrastructure to meet the challenges of rising consumption and evolving energy needs.

New Technologies and Smart Grid Adoption

Smart Grid Systems and Connected Devices

Smart metering is at the heart of grid modernization efforts across Latin America. The number of installed smart electricity meters is projected to grow at an annual rate of 23.5%, increasing from 17.3 million units in 2024 to 61.3 million by 2030. During this period, regional penetration is expected to rise from 7.7% to 24.8%. Brazil and Mexico lead the demand, accounting for over 65% of annual electricity meter installations. Despite Brazil serving 94 million electricity users, its smart meter penetration was only 6.5% in 2024, highlighting the immense growth potential in the coming years. By 2030, Brazil is expected to dominate the market, accounting for over half of all smart meter shipments in the region. Initiatives like those from Eletrobras and C3 AI, set to launch in early 2026, aim to leverage AI for advanced grid management.

One of the main drivers behind these investments is the need to combat non-technical losses, such as energy theft. For instance, Honduras installed over 500,000 smart meters by the end of 2024 to tackle this issue. Meanwhile, Uruguay achieved near-complete smart metering coverage by December 2024.

To ensure reliable data transmission, advanced communication technologies like Multiprotocol Label Switching (MPLS) are being adopted. In Brazil, Neoenergia is implementing MPLS to enhance the efficiency and reliability of power distribution data transmission. Other utility groups, including Cemig, COPEL, Enel, and CPFL in Brazil, as well as Grupo EPM and Enel in Colombia, and CFE in Mexico, are also driving these upgrades. These technological advancements are critical for integrating renewable energy sources, as smart systems play a vital role in maintaining grid stability.

Renewable Energy Integration

Incorporating renewable energy into the grid requires specialized equipment to manage bidirectional power flows and handle rapid load changes. As solar and wind installations expand across the region, utilities are increasingly pairing these renewable sources with Battery Energy Storage Systems (BESS) to ensure grid stability. For example, in December 2025, Chilean renewable platform T Power secured $325 million to develop a 141-MW/677 MWh battery energy storage system alongside a 141-MW solar project. Similarly, Iberdrola launched the Noronha Verde project in Brazil in November 2025, which includes a 22-MWp solar plant paired with a 49-MWh battery storage system. Another noteworthy project, the Luiz Carlos Solar Park in Brazil, was commissioned by Atlas Renewable Energy in December 2025. This 315-MW facility, equipped with 516,000 bifacial modules, will supply renewable electricity to ArcelorMittal’s industrial operations.

These projects depend on advanced components like communication-enabled circuit breakers and digital protection relays, which are essential for sophisticated grid management. Companies looking to support renewable integration projects can turn to platforms like Electrical Trader, which provides a wide range of critical equipment, including transformers and switchgear. These efforts demonstrate how modernized power distribution systems are essential to advancing the region's energy transition.

Country-Specific Trends and Market Leaders

After exploring regional market dynamics and technology adoption, let's dive into the country-specific trends shaping the power distribution sector.

Brazil: Electrification and Market Leadership

Brazil stands out as a leader in electrification and investment, commanding 37.7% of the regional market in 2024. The country has made significant strides in connecting new residential areas to the grid, driven by both public and private funding. For instance, the National Electric Energy Agency (ANEEL) has allocated BRL 2.5 billion (around $500 million) toward smart metering and automated grid monitoring systems.

Local manufacturers are also ramping up production. Hitachi Energy, for example, began constructing a new transformer factory in Pindamonhangaba in August 2025. This $200 million project aims to double domestic production capacity by 2028.

Brazil is addressing challenges in remote electrification with innovative projects like the Vila Restauração microgrid in the Amazon. Completed in 2025, this system uses 829 kWh lithium battery packs and a 325 kW solar array to replace traditional medium-voltage feeders, providing reliable power to an entire village.

Mexico: Industrial Expansion and EV Infrastructure

Mexico is the fastest-growing market for power transmission and distribution equipment in Latin America, with projected revenues of $6.3 billion by 2030. The power and distribution transformer segment alone is set to grow at a CAGR of 8.64% through 2030. This growth is largely driven by industrial expansion, with the Federal Electricity Commission focusing on major infrastructure upgrades to ensure grid stability.

The rise of electric vehicles (EVs) is also transforming Mexico's distribution networks. In 2023 and 2024, the National Commission for the Efficient Use of Energy (CONUEE) mandated ultra-fast DC charging stations on major highways. These stations require specialized transformers and smart meters to handle high-voltage demands. To further support industrial digitalization, Schneider Electric opened a technical service center in Guadalajara in May 2023, offering local engineering support for smart distribution panels and motor control centers.

Chile, Colombia, and Argentina: Emerging Opportunities

Argentina is set to achieve the highest CAGR in the power transmission and distribution market from 2025 to 2030, despite facing economic challenges. However, foreign exchange controls imposed by the Central Bank have complicated the import of essential components like circuit breakers and digital protection relays.

In Chile, transmission bottlenecks on 69–138 kV lines led to the curtailment of 2,375 GWh of solar and wind energy in 2023. To address this, T Power secured $325 million in December 2025 to develop a 141-MW/677 MWh battery energy storage system alongside a 141-MW solar project, aimed at improving grid reliability. Additionally, the demand for medium-voltage switchgear and high-efficiency systems is growing, particularly in remote mining regions.

Colombia is focusing on smart grid adoption, mandating the use of Intelligent Electronic Devices (IEDs) in new distribution nodes to enhance fault detection. As part of its push for digitalized power distribution, the government approved COP 8.35 trillion (about $2.1 billion) in October 2025 for the "Colombia Solar" program. This initiative aims to equip 1.3 million low-income households with rooftop PV systems by 2030. In December 2025, the Ministry of Mines and Energy launched the Gecelca Solar project, starting with a 650 MW solar portfolio to lower electricity costs for over 150,000 households.

Renewable Energy Integration and Electrification Challenges

Hydropower and Renewable Energy Expansion

Latin America's power sector has seen a major shift, but adapting the grid to handle this transformation is proving challenging. By late 2025, 71% of the region's electricity came from renewable sources, up from 68% in 2024. Hydropower accounted for 45%, solar and wind made up 18%, and natural gas filled 27% of the mix, providing stability during droughts or periods of high demand.

The rapid growth of solar and wind energy is pushing aging transmission networks to their limits, leading to generation cuts in some areas. To tackle this, Brazil has invested over $10.5 billion in transmission concessions since 2023 to upgrade its grid.

"You can't electrify the future on yesterday's grid. Latin America's success won't be measured in megawatts installed, but in megawatts delivered." - Inês Gaspar, Research Lead for Latin America, Aurora Energy Research

Permitting delays are another hurdle. Transmission line projects typically take 7–10 years to complete, with 60% of that time spent on permitting. To address this bottleneck, Chile introduced its 2024 Energy Transition Law, which accelerates key grid projects while maintaining environmental protections. Meanwhile, Mexico now requires new renewable projects to include battery storage for grid stability. These efforts aim to modernize the grid, but they also highlight the broader challenges of electrifying remote and underserved areas.

Rural Electrification Barriers

While centralized grids are being upgraded to accommodate renewables, extending electricity to remote areas remains a tough challenge. Even with an average electricity access rate of 97% across Latin America, around 17 million people still lack power. Geographic isolation, particularly in places like the Amazon, makes traditional grid expansion both technically and economically impractical. On top of that, grid losses in the region average 16%, far higher than the 6% seen in OECD countries, further discouraging utilities from investing in remote infrastructure.

Decentralized energy solutions are helping to fill the gap. In 2025, Brazil's Reservas Extrativistas initiative swapped out diesel generators for solar photovoltaic systems with storage in the Amazon. This project not only stabilized electricity for cold storage - boosting local fish production - but also trained community members to monitor and maintain the systems. Similarly, São Paulo's Unicamp University operates a government-funded microgrid with 565 kWp of solar power and a 1 MW/2 MWh battery system, cutting annual energy costs by about BRL 450,000 (roughly $83,000) as of December 2025.

In Rio de Janeiro's favelas, the RevoluSolar program uses a cooperative model to bring net metering to low-income households. By the end of 2025, the initiative had trained over 20 local residents as electricians and solar installers to maintain these decentralized networks. These projects show that rural electrification isn't just about infrastructure - it's about empowering communities through local ownership and technical training.

Conclusion: 2026 Trends and Future Outlook

Latin America's power distribution market is set for a major transformation in 2026, with electrical infrastructure upgrades taking center stage. The power distribution component market is projected to hit USD 58.83 billion by 2025, fueled by a 7.58% compound annual growth rate (CAGR). Brazil leads the charge with 37.7% of the market, while Mexico is on track for a 4.78% CAGR through 2031, driven by industrial near-shoring and the rise of hyperscale data centers.

Digitalization is reshaping the industry, as utilities increasingly demand sensor-enabled transformers and IEC 61850 automation systems to enable predictive maintenance and self-healing grids. These digital-ready units, which help reduce downtime and extend asset life, carry a 6%–9% price premium. With over 40% of the region's electrical distribution assets exceeding 30 years in age, the push for accelerated replacement cycles is creating opportunities. However, logistics costs - especially in remote areas - can account for as much as 30% of final equipment prices, making sourcing strategies even more critical.

For companies needing transformers, switchgear, circuit breakers, and other components, strategic procurement is key. Platforms like Electrical Trader simplify access to certified new, used, and surplus equipment, offering solutions for everything from urban grid upgrades to remote microgrid installations. As market conditions and regulations evolve, this kind of agile sourcing becomes indispensable.

Beyond sourcing, businesses must adapt to changing regulations, such as Mexico's National Energy Commission tenders and Brazil's ANEEL innovation agenda. Prioritizing equipment that supports renewable energy integration is essential, reflecting the region's broader push to modernize aging infrastructure while advancing sustainability goals. Success in 2026 will hinge on a combination of technical expertise and flexible sourcing strategies to meet the region's evolving energy needs.

FAQs

What upgrades cut grid losses the fastest?

Smart meters and grid-enhancing technologies offer a fast track to cutting down grid losses. These upgrades allow for better system monitoring, improve operational efficiency, and optimize transmission performance. By adopting these tools, utilities can tackle inefficiencies head-on and improve overall grid management.

How do smart meters reduce energy theft?

Smart meters play a key role in cutting down energy theft by providing real-time tracking of electricity usage. With these devices, utilities can pinpoint unusual consumption patterns and spot unauthorized connections. This makes it much easier to prevent power losses while ensuring billing remains accurate.

What equipment is needed for renewables and batteries?

Renewable energy systems and battery setups rely on several key pieces of equipment. These include solar panels, wind turbines, and energy storage systems such as batteries. Other essential components are inverters, charge controllers, and power conversion devices. Together, these elements work to seamlessly integrate renewable energy sources into the power grid.